Summary: Prices received by producers tumble; fall much more than expected; driven by 56.6% fall in petrol price; federal funds rate forecast to fall in 2021 despite Fed reluctance.

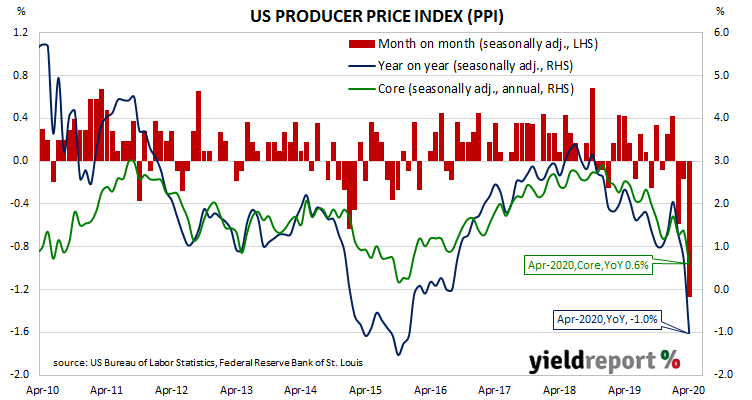

Around the end of 2018, the annual inflation rate of the US producer price index (PPI) began a downtrend which then continued through 2019. Months in which prices received by producers increased suggested the trend may have been coming to an end, only for it to continue. There’s really no doubt now.

April figures published by the Bureau of Labor Statistics indicate producer prices dropped by 1.3% after seasonal adjustments. The fall was much harder than the 0.4% decline which had been generally expected and considerably larger in magnitude than March’s -0.2%. On a 12-month basis, the rate of producer price inflation after seasonal adjustments reversed at 1.0% after recording 0.7% in March and 1.3% in February.

“Core” PPI inflation fell by 0.3%, more than just reversing March’s 0.2% increase. The annual rate more than halved from 1.4% to 0.6%.

US Treasury bond yields finished a little lower. By the end of the day, the US 2-year Treasury yield finished unchanged at 0.16% while 10-year and 30-year yields each shed 2bps to 0.65% and 1.35% respectively.

Expectations of any change in the federal funds rate over the next 12 months remained negligible, especially after a speech given by US Fed chief Jerome Powell later that same day. However, OIS contracts from March 2021 onwards continued to imply a zero effective federal funds rate.