Summary: Value of loan commitments up 4.8% in May; 20.5% lower than May 2022; UBS: figures imply housing credit growth will ease further; ANZ: average owner-occupier mortgage for existing homeowners a touch higher, average first home buyer mortgage sharply lower; value of owner-occupier loan approvals up 4.0%; investor approvals up 6.2%; number of home loan approvals up 5.1%.

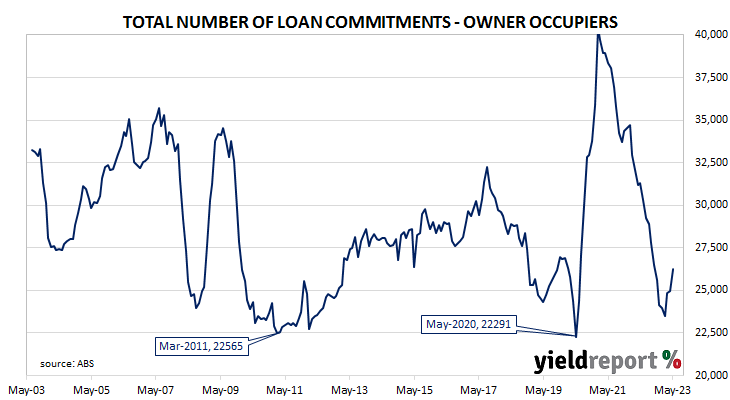

The number and value of home-loan approvals began to noticeably increase after the RBA reduced its cash rate target in a series of cuts beginning in mid-2019, potentially ending the downtrend which had been in place since mid-2017. Figures from February through to May of 2020 provided an indication the downtrend was still intact but subsequent figures then pushed both back to elevated levels in 2021. However, there has been a considerable pullback since then.

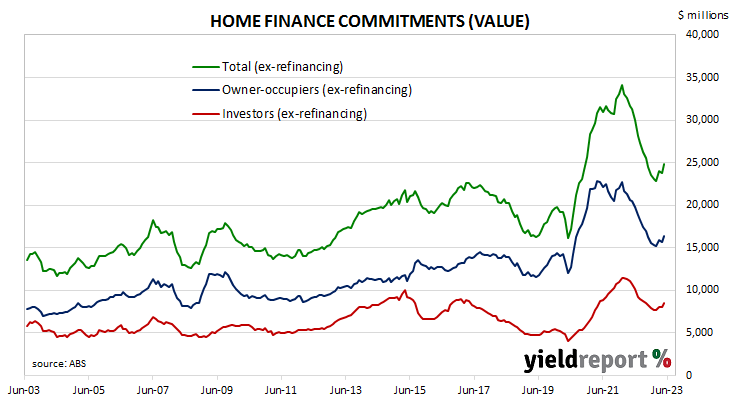

May’s housing finance figures have now been released and total loan approvals excluding refinancing increased by 4.8% In dollar terms over the month, slightly more than the 4.0% increase which had been generally expected and in contrast with April’s 1.0% fall. On a year-on-year basis, total approvals excluding refinancing fell by 20.5%, up from the previous month’s comparable figure of -25.1%.

“Home loans have bounced in recent months but still imply housing credit growth will ease a bit further over coming months towards [about] 4% year-on-year,” said UBS economist George Tharenou.

The figures came out on the same day as several other reports and Commonwealth Government bond yields fell noticeably. By the close of business, 3-year and 10-year ACGB yields had both decreased by 6bps to 3.93% and 3.96% respectively while the 20-year yield finished 8bps lower at 4.22%.

In the cash futures market, expectations regarding further rate rises softened. At the end of the day, contracts implied the cash rate would rise from the current rate of 4.07% to average 4.135% in July and then to 4.275% in August. February 2024 contracts implied a 4.505% average cash rate while May 2024 contracts implied 4.45%, 38bps more than the current rate.

“Compared to a year ago, the average owner occupier mortgage for existing homeowners is a touch higher while the average first home buyer mortgage is sharply lower, likely due to affordability constraints for those who had not benefitted from previous housing price increases,” said ANZ senior economist Adelaide Timbrell. “External refinancing is just 1% off its March 2023 peak and may signal that borrowers are shopping around on mortgage rates, reducing the impact of monetary tightening on interest payments.”

The total value of owner-occupier loan commitments excluding refinancing increased by 4.0%, a turnaround from April’s 1.4% fall. On an annual basis, owner-occupier loan commitments were 20.2% lower than in May 2022, above April’s comparable figure of -23.5%.

The total value of investor commitments excluding refinancing arrangements increased by 6.2%. The rise followed a 0.2% decline in April, slowing the contraction rate over the previous 12 months from 28.1% after revisions to 20.9%.

The total number of loan commitments to owner-occupiers excluding refinancing increased by 5.1% to 26,253 on a seasonally adjusted basis. The rise was larger than April’s 0.5% increase and the annual contraction rate slowed from 19.9% to 16.2%.