Summary: Value of loan commitments down 1.0% in June, contrasts with expected gain; 18.2% lower than June 2022; Westpac: clear up-trend led by prices, volumes relatively flat; UBS: trend implies housing/total credit growth will ease a bit further; value of owner-occupier loan approvals down 2.8%; investor approvals up 2.6%; number of owner-occupier home loan approvals down 3.0%.

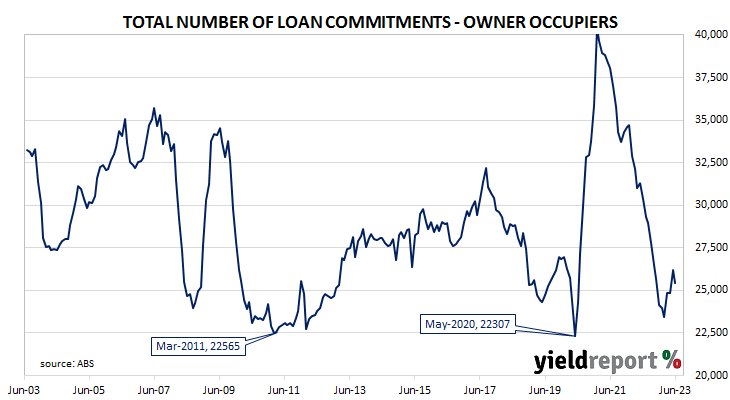

The number and value of home-loan approvals began to noticeably increase after the RBA reduced its cash rate target in a series of cuts beginning in mid-2019, potentially ending the downtrend which had been in place since mid-2017. Figures from February through to May of 2020 provided an indication the downtrend was still intact but subsequent figures then pushed both back to elevated levels in 2021. However, there has been a considerable pullback since then.

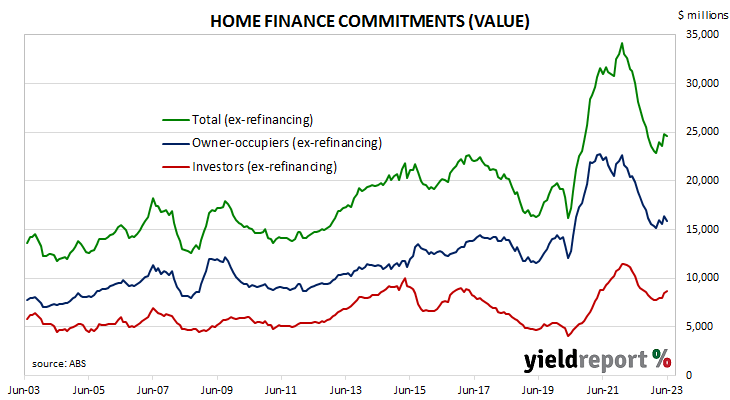

June’s housing finance figures have now been released and total loan approvals excluding refinancing declined by 1.0% In dollar terms over the month, as opposed to the 1.8% increase which had been generally expected and May’s 5.4% rise. On a year-on-year basis, total approvals excluding refinancing fell by 18.2%, up from the previous month’s comparable figure of -20.5%.

“Despite the dip, approvals remain on a clear up-trend, having risen 7.6% from their February low,” said Westpac senior economist Matthew Hassan. “However, that gain is being led by prices with volumes still relatively flat to date.”

The figures came out on the same day as the latest dwelling approval figures and the August RBA Board meeting. Commonwealth Government bond yields fell noticeably and, by the close of business, the 3-year ACGB yield had shed 12bps to 3.74% while 10-year and 20-year yields both finished 9bps lower at 3.97% and 4.27% respectively.

In the cash futures market, expectations regarding further rate rises softened. At the end of the day, contracts implied the cash rate would rise from the current rate of 4.07% to average 4.105% in September and then to 4.145% in October. February 2024 contracts implied a 4.22% average cash rate and May 2024 contracts implied 4.195%, around 12bps more than the current rate.

UBS economist George Tharenou generally agreed with his Westpac counterpart. “The trend over recent months is still rising moderately and is consistent with home prices rising but [it] still implies housing (and total) credit growth will ease a bit further over coming months towards around 4% year-on-year.”

The total value of owner-occupier loan commitments excluding refinancing decreased by 2.8%, a turnaround from May’s 5.1% rise. On an annual basis, owner-occupier loan commitments were 19.9% lower than in June 2022, above May’s comparable figure of -20.2%.

The total value of investor commitments excluding refinancing arrangements increased by 2.6%. The rise followed a 5.9% increase in May, slowing the contraction rate over the previous 12 months from 21.1% after revisions to 15.0%.

The total number of loan commitments to owner-occupiers excluding refinancing decreased by 3.0% to 25,412 on a seasonally adjusted basis. The fall contrasted with May’s 5.6% increase and the annual contraction rate ticked up from 16.2% to 16.3%.