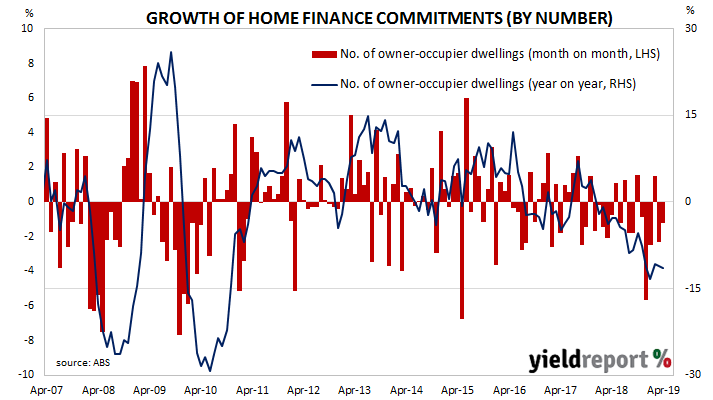

Since late 2017/early 2018, a very clear downtrend has been evident in the monthly figures of both the number and value of home loan commitments. After the figures from February were released, some economists speculated the worst may have been over. The latest numbers have not contradicted that assertion but nor have they really bolstered the case.

The ABS has released April’s housing finance commitment figures and they were less than expected. The total number of loan commitments to owner-occupiers fell by 1.2%, a larger contraction than the expected -0.3% and a continuation of March’s revised figure of -2.3%. On an annual basis, the growth rate further deteriorated from March’s revised figure of -11.0%, recording -11.5%. When “re-financings” are removed, the number of loan commitments fell by 1.1% over the month and by 13.5% when compared to commitments from April 2018.

Westpac senior economist Matthew Hassan described the result as “disappointing” but understandable given “the material improvement that has occurred since the Federal election and the prospective shift that is likely to come following the recent interest rate cut.”

ANZ economist Adelaide Timbrell went a little further, stating the figures represented “green shoots”. While she acknowledged “annual results are still showing substantial declines…” she noted “…these declines have been shrinking in the last few months.” She also suggested the federal election and the timing of holidays may have had some bearing on investor figures.

UBS economist George Tharenou agreed in part, at least with “the worst is over” approach. However, he saw some reasons to be cautious. “Looking forward we still see headwinds of tight credit from higher HEM (Household Expenditure Measure) benchmarks and increased verification, the roll out of Comprehensive Credit Reporting and potential Debt-To-Income limits, meaning we don’t expect a sharp reflation of housing in the near-term.”