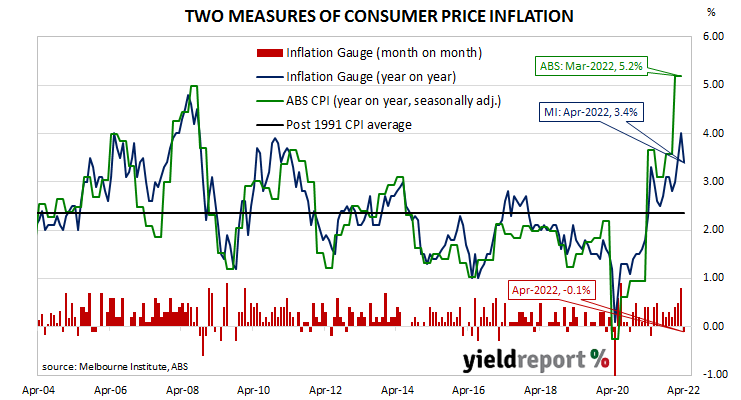

Summary: Melbourne Institute Inflation Gauge index down 0.1% in April; up 3.4% on annual basis; fall largely associated recent fuel price decline; inflation to remain elevated in short term”, moderate in coming quarters.

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge and the CPI have diverged for as long as twelve months. On average, the Inflation Gauge’s annual rate tends to overestimate the ABS rate by around 0.1%.

The Melbourne Institute’s latest reading of its Inflation Gauge index indicates consumer inflation declined by 0.1% in April. The rise follows increases of 0.8% in March and 0.5% in February. On an annual basis, the index rose by 3.4%, down from 4.0% in March.

“The fall in headline inflation for April is largely associated with a recent decline in fuel prices, which surged in February and March. In contrast, housing-related costs continued to rise in April,” said the Melbourne Institute’s Associate Professor Sam Tsiaplias.

The figures were released at roughly the same time as ANZ’s latest Job Ads report but the effect of either on Commonwealth Government bond yields were overshadowed by jumps in US Treasury yields on Friday night. By the close of business, the 3-year ACGB yield had gained 12bps to 2.86%, the 10-year yield had leaped 14bps to 3.31% while the 20-year yield finished 12bps higher at 3.57%.

In the cash futures market, expectations of any material change in the actual cash rate, currently at 0.06%, softened a touch. At the end of the day, contract prices implied the cash rate would rise to 0.195% in May and then move to 1.315% in August. February 2023 contracts implied a cash rate of 2.79%.

Tsiaplias expects inflation rates to “remain elevated in the short term” but “likely moderate in coming quarters, even without aggressive monetary policy.” He said the March quarter’s “spike” was largely attributable to fuel price rises and “supply-side constraints” in the housing market.