The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower and it has been below the RBA’s target band for some years now. Despite the RBA’s desire for a higher inflation rate, attempts to accelerate inflation through record-low interest rates have failed to date.

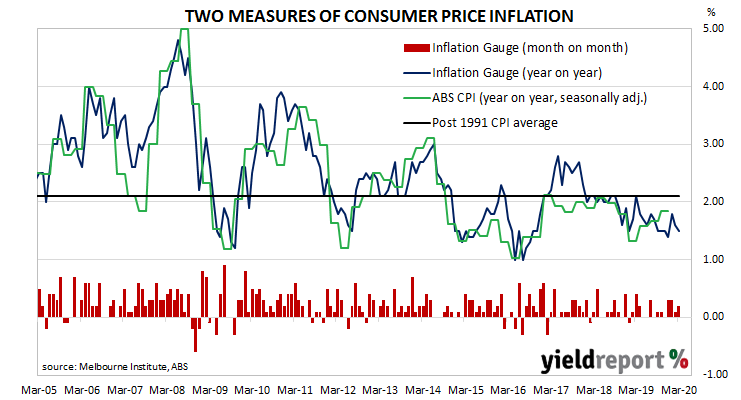

The Melbourne Institute’s latest Inflation Gauge index increased by 0.2% through March following a 0.1% increase in February and +0.3% in January. On an annual basis, the index increased by 1.5%, down from February’s comparable rate of 1.6%.

Domestic bond yields generally moved a touch higher. By the end of the day, 3-year and 10-year ACGB yields had each inched 1bp higher to 0.25% and 0.76% respectively while the 20-year yield finished 3bps higher at 1.44%.

Prices of cash futures contracts hardly moved. By the end of the day, April contracts implied a rate cut down to zero as a 57% chance, up from the previous day’s 55%. May contracts implied a 52% chance of such a move in that month, the same likelihood as at the end of the previous day. Another rate reduction was not seen as being any more likely in later months of 2020; December contracts implied a 49% chance of a rate cut down to zero.

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge and the CPI have diverged for as long as twelve months. On average, the Inflation Gauge’s annual rate tends to overestimate changes in CPI inflation by an average of about 0.1%.