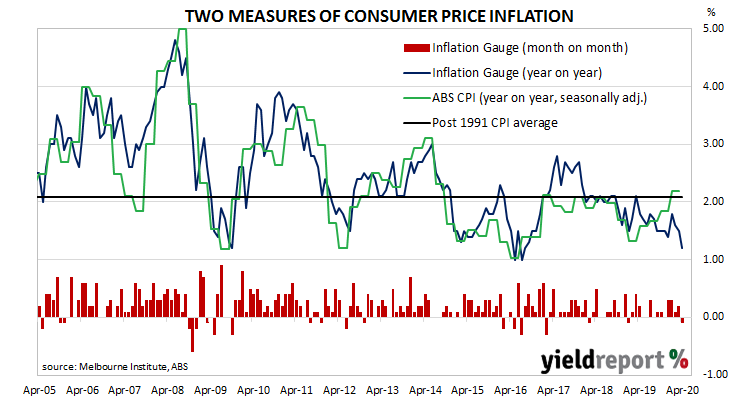

The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower and it has been below the RBA’s target band for some years now. Despite the RBA’s desire for a higher inflation rate, attempts to accelerate inflation through record-low interest rates have failed to date.

The Melbourne Institute’s latest Inflation Gauge index decreased by 0.1% through April. The small decline follows a 0.2% increase in March and a 0.1% increase in February. On an annual basis, the index increased by 1.5%, down from March’s comparable rate of 1.6%.

The index came out on the same day as ANZ’s Job Ads report and March’s dwelling approval numbers. Commonwealth bond yields moved lower, although they finished largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had slipped 1bp to 0.24%, the 10-year yield had lost 3bps to 0.83% while the 20-year yield finished 4bps lower at 1.46%.

In the cash futures market, expectations of a rate cut softened a touch. By the end of the day, May contracts implied a rate cut down to zero as a 60% chance, down from the previous day’s 62%. June contracts implied a 56% chance of such a move in that month, down from 58%. Contract prices of months in the remainder of 2020 and through to mid-2021 implied similar probabilities, ranging between 45% and 65%.