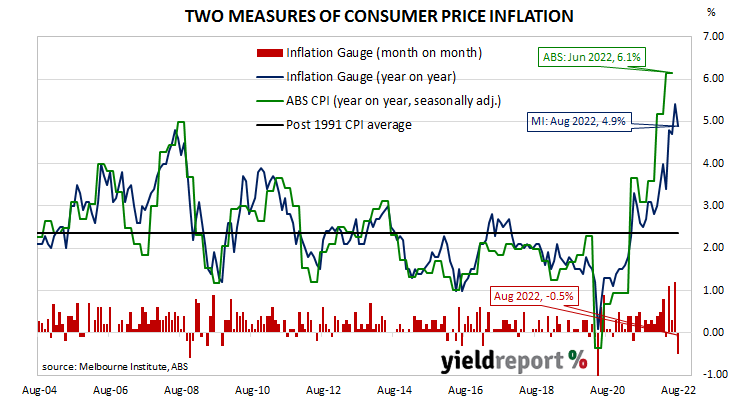

Summary: Melbourne Institute Inflation Gauge index down 0.5% in August; up 4.9% on annual basis.

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge and the CPI have diverged for as long as twelve months. On average, the Inflation Gauge’s annual rate tends to overestimate the ABS rate by around 0.1%.

The Melbourne Institute’s latest reading of its Inflation Gauge index indicates consumer prices decreased by 0.5% in August. The fall follows increases of 1.2% and 0.3% in July and June respectively. On an annual basis, the index rose by 4.9%, down from 5.4% in July.

“The results suggest ongoing, broad-based inflationary pressure with higher prices observed for a wide range of goods and services, including utilities, rents, housing construction, food and insurance,” said the Melbourne Institute’s Associate Professor Sam Tsiaplias.

The figures were released on the same day as ANZ’s latest job advertisement report and Commonwealth Government bond yields were largely unchanged except at the ultra-long end. By the close of business, the 3-year ACGB yield had slipped 1bp to 3.31%, the 10-year yield had returned to its starting point 3.66% while the 20-year yield finished 4bps higher at 3.98%.

In the cash futures market, expectations of higher rates softened slightly. At the end of the day, contracts implied the cash rate would rise from the current rate of 1.81% to 2.18% in September, increase to 2.59% in October and then to 2.965% in November. May 2023 contracts implied a 3.775% cash rate and August 2023 contracts implied 3.84%.

Central bankers desire a certain level of inflation which is “sufficiently low that it does not materially distort economic decisions in the community” but high enough so it does not constrain “a central bank’s ability to combat recessions.” Hence the recent obsession among central banks, including the RBA, to bring inflation back to their various targets.