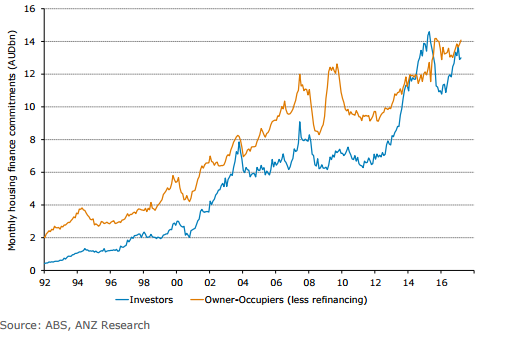

Some economists and analysts argue an expansion of credit is the main driver of house price inflation and assets in general. Even the RBA acknowledges* an association of house price growth with access to finance. They also argue there are other factors at work such as population, household size and inflation as well but “access to finance” cannot be ignored. Monthly housing finance figures are thus viewed as an indicator of continuing trends and also of turning points.

The ABS has released housing finance figures for March and the figures indicate the number of owner-occupier approvals fell 0.5% when compared to February and they are 1.9% less than in March 2016. However, excluding refinancing, the number of approvals was the same as February and 3.8% higher than a year ago. These figures were largely in line with market expectations.

In dollar terms, owner-occupier loan approvals increased by 0.9% in March, a turnaround from the 0.7% fall in February. Compared to March 2016 loans of this type were 0.3% higher. Investor loan growth grew by 0.8% in March but compared to 12 months ago they are 14.2% higher, which represents an acceleration from February’s year-on-year figure of 13.8%. Total loan approvals excluding refinancing was 10% higher than March 2016, exactly the same rate as the maximum housing credit growth designated by APRA.

The macro-prudential curbs introduced in 2015 seem to have lost their effectiveness. Additional restrictions have been introduced by APRA in late March but as Westpac’s senior economist Matthew Hassan said “the exact impact of new regulatory guidelines is unclear. The specific limit for investor credit growth was unchanged at 10% although lenders were instructed to keep growth ‘comfortably below’ the target.”

Unless you have been living in an underground bunker, then you will know Australian property prices on average have been red hot and they are considerably higher than they were five or ten years ago. However, the reality is prices have gone backwards recently in some cities and it is the price of housing in the three most-populated cities in the country which have pushed the average Australian price higher. This latest round of tighter lending standards is not expected to show up in lending figures until next month or later but if Australia truly does have a house price bubble, nothing will make any difference in any case until the herd unexpectedly changes direction.

*“…cheaper and easier access to finance underpinned a secular increase in households’ debt-to-income ratio that was closely associated with high housing price inflation from the early 1990s until the mid-2000s.” RBA Bulletin September quarter 2015, Long-run Trends in Housing Price Growth, Marion Kohler and Michelle van der Merwe.