Summary: ISM PMI recovers a little; manufacturing still deep in contraction territory; overall economy barely growing; supply times “flatter” index.

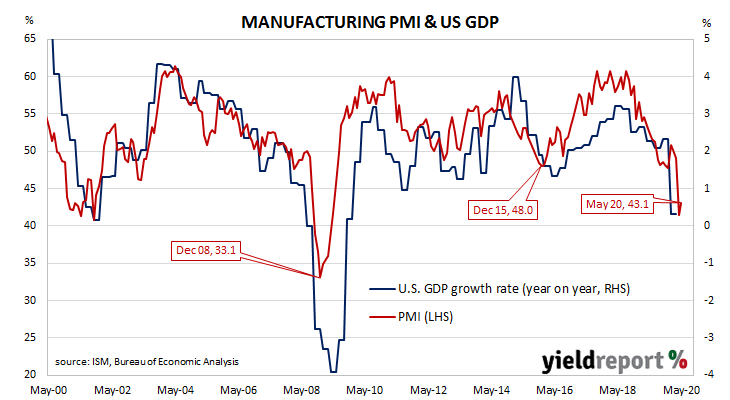

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. Readings stabilised in late 2019 after a truce of sorts was made with the Chinese regarding trade. However, the March 2020 report implied US manufacturing activity had begun contracting and then April’s report confirmed it.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 43.1% in May. The result was a little under the expected figure of 43.8% but also a little higher than April’s final reading of 41.5%. The average reading since 1948 is 52.8% and any reading below 50% implies a contraction in the manufacturing sector. However, a reading “above 42.8%, over a period of time, generally indicates an expansion of the overall economy,” according to the ISM.

The ISM’s Tim Fiore said the path of the manufacturing sector’s contraction had “improved”, implying its rate of contraction had lessened. However, he noted it was still at April 2009 levels. US Treasury yields increased at the ultra-long end of the curve but barely moved elsewhere. By the end of the day, the 2-year Treasury bond yield had slipped 1bp to 0.15% while the 10-year yield had ticked up 1bp to 0.66% and the 30-year yield finished 4bps higher at 1.45%.

US Treasury yields increased at the ultra-long end of the curve but barely moved elsewhere. By the end of the day, the 2-year Treasury bond yield had slipped 1bp to 0.15% while the 10-year yield had ticked up 1bp to 0.66% and the 30-year yield finished 4bps higher at 1.45%.

After April’s reading was released, NAB head of FX Strategy within its FICC division Ray Attrill had said the index had been “held up” by a lengthier-than-usual supplier delivery times which he analysed as a product of “disrupted supply chains…” rather than a sign of demand outstripping supply. He noted this influence on the index again, saying the index reading “was once again flattered by the strength of the supplier deliveries sub-index…”