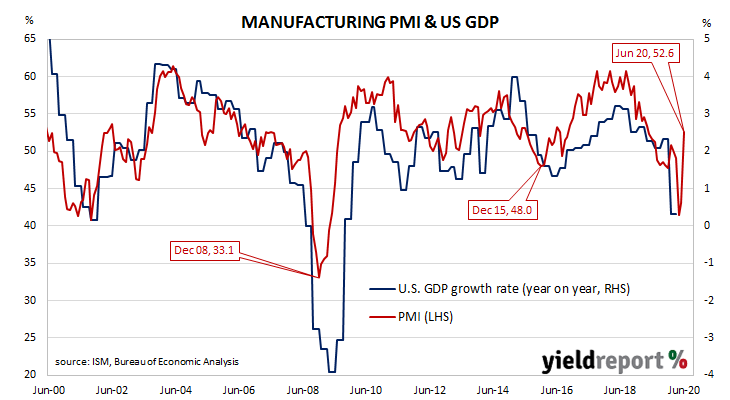

Summary: ISM purchasing managers index jumps above 50; manufacturing back into expansionary territory; implies US economy growing at solid rate; recent US infection rates may prompt “set-backs” in coming months.

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. Readings stabilised in late 2019 after a truce of sorts was made with the Chinese regarding trade. March’s report signalled a contraction in US manufacturing activity had begun which deepened through April and May.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 52.6% in June. The result was above the expected figure of 49.0% and considerably higher than May’s final reading of 43.1%. The average reading since 1948 is 52.9% and any reading above 50% implies an expansion in the manufacturing sector. A reading “above 42.8%, over a period of time, generally indicates an expansion of the overall economy,” according to the ISM.

“A reading of 52.6 for the ISM Manufacturing Index indicates the US economy is rapidly recovering,” said ANZ economist Daniel Been.

The report was released on the same day as the ADP June report and US Treasury yields rose modestly. By the close of business, the 2-year Treasury bond yield had gained 4bps to 0.17%, the 10-year yield had increased by 3bps to 0.68% while the 30-year yield finished 1bp higher at 1.42%.

NAB head of FX Strategy (FICC division) Ray Attrill said, “As always, being a diffusion indices ISM/PMI surveys need to be interpreted with caution being a ‘rate of change’ metric that says nothing directly about levels of activity.” He also noted many US states had either stalled or reversed easings of restrictions which could prompt “set-backs in some of these readings in coming months…”

Purchasing Managers’ Indices (PMIs) are economic indicators derived from monthly surveys of executives in private-sector companies. They are diffusion indices, which means a reading of 50% represents no change from the previous period, while a reading under 50% implies respondents reported a deterioration on average. They are particularly useful as a leading indicator.