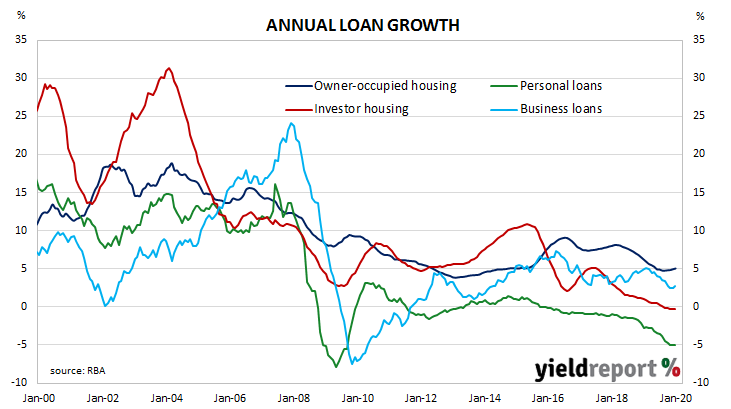

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. It appeared to have stabilised in the September quarter of 2018 but the annual growth rate then continued to deteriorate through 2019, despite some optimism emerging in the housing market following the re-election of the Coalition Government in May of that year.

While senior RBA officials would like business lending to increase, those same officials would also like households to reduce debt. Recently, RBA Governor Philip Lowe publicly stated the cash rate has been reduced in part to assist households to set aside funds to repay debt.

According to the latest RBA figures, private sector credit grew by +0.3% in January, just above the +0.2% increase which had been expected as well as December’s +0.2% increase. The annual growth rate ticked up from 2.4% to 2.5%.

The increase over the month was predominantly driven by increased business lending, with real estate investors also playing a significant part. Personal lending contracted again while lending to owner-occupiers increased modestly. Westpac senior economist Andrew Hanlan said, “Credit began 2020 on a slightly better note, expanding by 0.33% in January; while not strong, that is the best monthly outcome since October 2018.” He noted a “turnaround in the housing sector is evident.”

Westpac senior economist Andrew Hanlan said, “Credit began 2020 on a slightly better note, expanding by 0.33% in January; while not strong, that is the best monthly outcome since October 2018.” He noted a “turnaround in the housing sector is evident.”

Local financial markets reacted by sending bond yields lower, although demand for bonds was almost certainly driven by a rush to safe assets as equity markets were hit by COVID-19 fears. By the end of the Australian trading day, the 3-year Treasury bond yield had lost 6bps to 0.50%, the 10-year yield had shed 4bps to 0.81% while the 20-year yield finished 3bps lower at 1.22%.