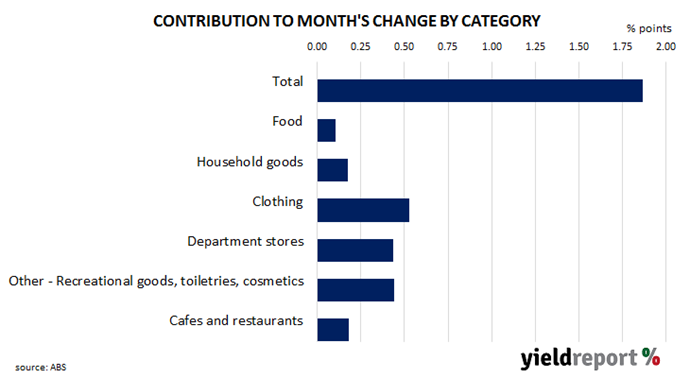

Summary: Retail sales up 1.9% in January, more than expected; households switching from retail towards discretionary services; underlying trend still shows slowdown; largest influence on result from clothing.

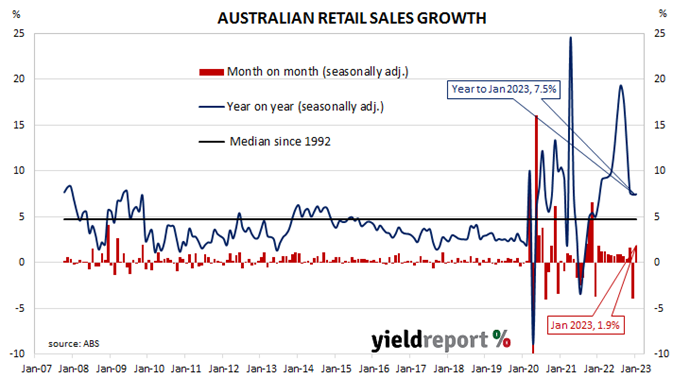

Growth figures of domestic retail sales spent most of the 2010s at levels below the post-1992 average. While economic conditions had been generally favourable, wage growth and inflation rates were low. Expenditures on goods then jumped in the early stages of 2020 as government restrictions severely altered households’ spending habits. Households mostly reverted to their usual patterns as restrictions eased in the latter part of 2020 and throughout 2021, although not for all categories.

According to the latest ABS figures, total retail sales rose by 1.9% in January on a seasonally adjusted basis. The rise was greater than the 1.5% increase which had been generally expected and in contrast with December’s revised figure of -4.0%. Sales increased by 7.5% on an annual basis, up a touch from December’s comparable figure of 7.4% after revisions.

“More households are switching consumption from retail towards discretionary services, like travel, which are not counted in retail sales,” said ANZ economist Madeline Dunk. “More broadly, we continue to expect consumption growth to slow in 2023, as rate rises and cost-of-living pressures eat into household budgets.”

Commonwealth Government bond yields moved lower on the day. By the close of business, the 3-year ACGB yield had shed 4bps to 3.61%, the 10-year yield had lost 2bps to 3.86% while the 20-year yield finished 1bp lower at 4.17%.

In the cash futures market, expectations regarding future rate rises softened. At the end of the day, contracts implied the cash rate would rise from the current rate of 3.32% to average 3.505% in March and then increase to an average of 3.935% through May. August 2023 contracts implied a 4.24% average cash rate while November 2023 contracts implied 4.275%.

“The rebound was better than expected coming off the choppy end of 2022 with November sales up 1.7% and December down 4%,” noted Westpac senior economist Matthew Hassan. “All industries experienced a rise in retail sales although the underlying trend still shows a slowdown, sales up just 0.1% over the 3 months to January compared to the 3 months to October.”

Retail sales are typically segmented into six categories (see below), with the “food” segment accounting for nearly 40% of total sales. However, the largest influence on the month’s total came from the clothing category where sales increased by 6.5% on average over the month and accounted for 0.5 percentage points of the net result.