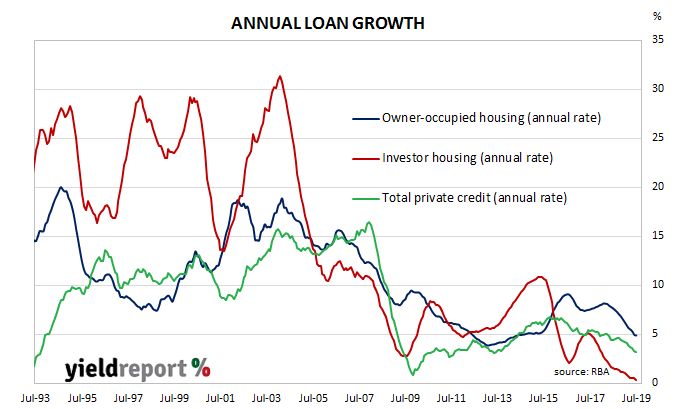

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. It appeared to have stabilised in the September quarter of 2018 but then subsequent credit figures put paid to that idea. However, the failure of the left-wing parties at the recent federal election and the consequent deferment of their policies has led to a noticeable increase in lending to owner occupiers.

According to the latest RBA figures, private sector credit grew by 0.2% in July, in line with expectations and up from May’s +0.1%. However, the annual growth rate slipped again, this time from June’s figure of 3.3% to 3.1% as lending to business remained subdued.

Financial markets reacted in a subdued fashion, although the release of July’s home approval figures will have had some effect as well. By the end of the day, 3-year ACGB yields remained unchanged at 0.67%, 10-year yields had inched up 1bp to 0.88% and 20-year yields remained unchanged at 1.29%. Cash futures prices moved to reduce the implied likelihood of further cuts in 2019 and 2020, although two more 25bps reductions are still expected. September contracts implied a 2% chance of a third rate cut for the year, down from the previous day’s 11%. October contracts implied a 13% chance of a third rate cut in 2019, down from 79%. November contracts finished with a rate cut priced as an 86% likelihood rather than being fully factored in but December contracts still have a 0.75% cash rate as a certainty.

Cash futures prices moved to reduce the implied likelihood of further cuts in 2019 and 2020, although two more 25bps reductions are still expected. September contracts implied a 2% chance of a third rate cut for the year, down from the previous day’s 11%. October contracts implied a 13% chance of a third rate cut in 2019, down from 79%. November contracts finished with a rate cut priced as an 86% likelihood rather than being fully factored in but December contracts still have a 0.75% cash rate as a certainty.