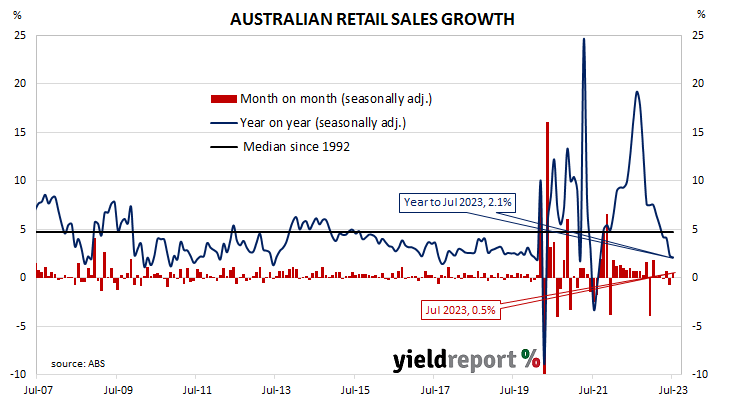

Summary: Retail sales up 0.5% in July, greater than expected; ANZ: little growth throughout 2023; ANZ: some upside in 2024; UBS: still weakening but not collapsing; largest influences on result from cafes/restaurants, department stores.

Growth figures of domestic retail sales spent most of the 2010s at levels below the post-1992 average. While economic conditions had been generally favourable, wage growth and inflation rates were low. Expenditures on goods then jumped in the early stages of 2020 as government restrictions severely altered households’ spending habits. Households mostly reverted to their usual patterns as restrictions eased in the latter part of 2020 and throughout 2021.

According to the latest ABS figures, total retail sales increased by 0.5% on a seasonally adjusted basis. The rise was greater than the generally-expected 0.2% increase and in contrast with an 0.8% fall in June. Sales increased by 2.1% on an annual basis, down from June’s figure of 2.3%.

“Despite rapid inflation, there’s been little growth in monthly retail sales throughout 2023, with the series only up 0.9% since January,” noted ANZ economist Madeline Dunk. “The underlying trend in retail sales along with our ANZ-observed spending data shows households are clearly cutting back.”

Long-term Commonwealth Government bond yields moved lower on the day, somewhat following movements of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had inched up 1bp to 3.86%, the 10-year yield had lost 2bp to 4.14% while the 20-year yield finished 4bps lower at 4.45%.

In the cash futures market, expectations regarding further rate rises eased. At the end of the day, contracts implied the cash rate would barely change from the current rate of 4.07% and average 4.075% in September and 4.095% in October. February 2024 contracts implied a 4.185% average cash rate while May 2024 contracts implied 4.205%, 14bps more than the current rate.

Economists, including ANZ’s Dunk, generally expect spending to further weaken in the short term before recovering in 2024. “We think households will continue to tighten their spending throughout 2023. We do, however, see some upside to spending in 2024 as inflation moderates and real household incomes turn positive.”

UBS economist George Tharenou agreed, at least in part. “Overall, our assessment of the consumer outlook, for now, remains a trend which is still weakening but not collapsing.”

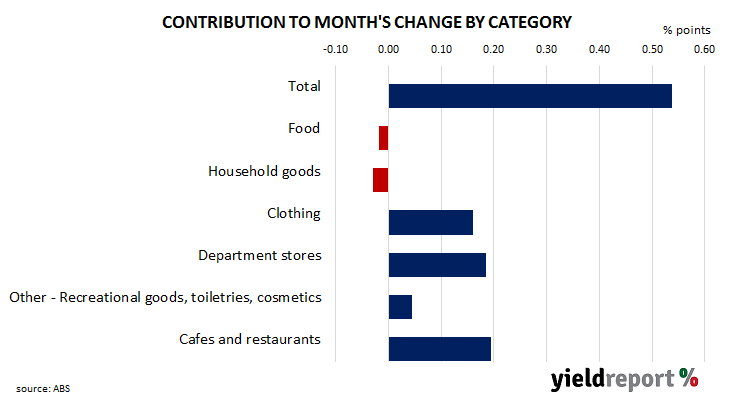

Retail sales are typically segmented into six categories (see below), with the “Food” segment accounting for 40% of total sales. However, the largest influences on the month’s total came from the “Cafes and restaurants” and “Department store” segments where sales rose by 1.3% and 3.6% respectively over the month.