Summary: Private capital expenditures down but better than expected; fall larger than in March quarter; points to sharp contraction in 2021/21; mining hold up, other sectors suffer larger drops; 2020/21 capex estimates noticeably lower than comparable estimates from 2019/20.

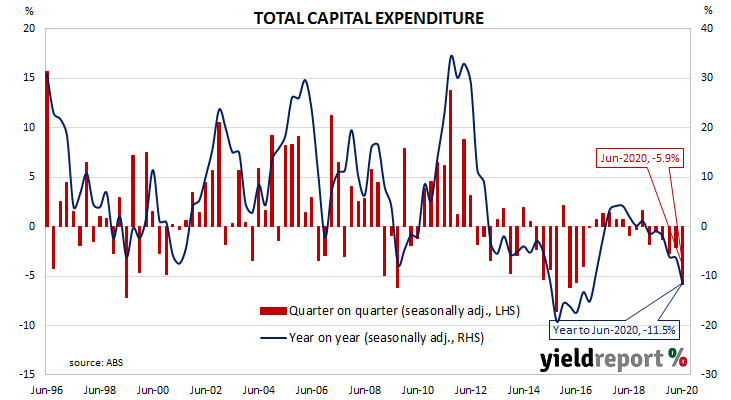

Australia’s capital expenditure (capex) slump was thought to be coming to an end as investment in the mining sector reverted back to its long-term mean after a spike early in the decade. Total investment had begun to grow again, driven by investment in the services sector. However, contractions in recent quarters have become the norm.

According to the latest ABS figures, seasonally-adjusted private sector capex in the June quarter fell by 5.9%. This latest figure was above the 7.9% contraction which had been expected but less than the March quarter’s revised figure of -2.1%. On a year-on-year basis, total capex contracted by 11.9% after recording an annual rate of -6.3% in the previous quarter after revisions.

“This latest update on capex plans point to a sharp contraction in business investment in 2020/21, as is to be expected in the current environment,” said Westpac senior economist Andrew Hanlan.

Long-term Commonwealth Government bond yields fell moderately. By the end of the Australian trading day, the 10-year Treasury bond yield had lost 3bps to 0.94% and the 20-year yield had shed 2bps to 1.50%. The 3-year yield remained unchanged at 0.31%.

In the cash futures market, expectations of any change in the actual cash rate, currently at 0.13%, continued to remain low. By the end of the day, contracts implied the cash rate would remain in a range from 0.115% to 0.12% through to the end of 2021.