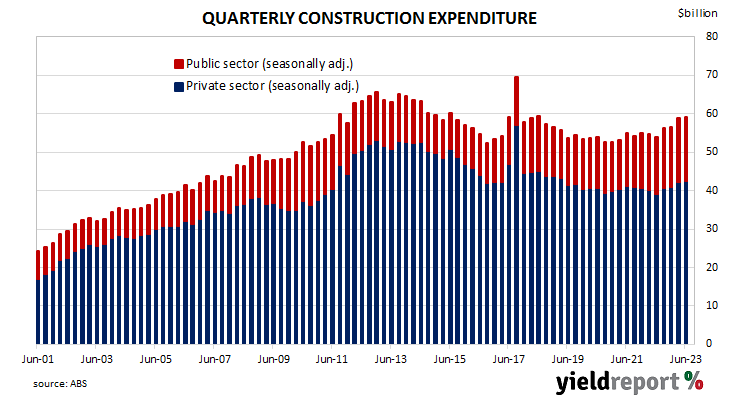

Summary: Construction spending up 0.4%, less than expected; ANZ: growth wanes after strong March quarter; Westpac: strength in part due to earlier delays; residential sector flat, non-residential building up 0.6%, engineering up 0.7%.

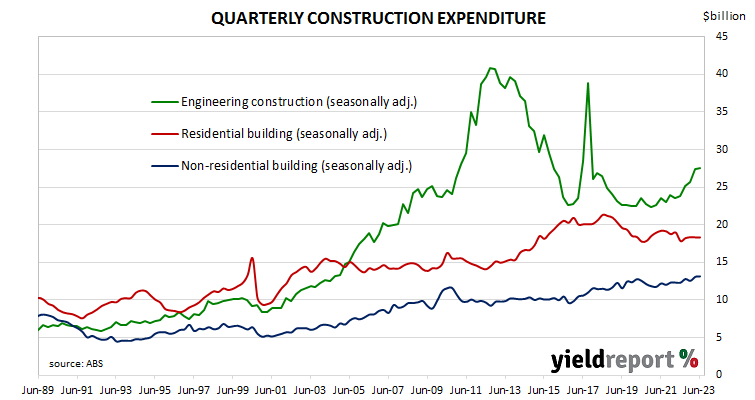

Construction expenditure increased substantially in Australia in the early part of last decade following a more-steady expansion through the 2000s. A large portion of the increase came from the commissioning of new projects and the expansion of existing ones to exploit a tripling in price of Australia’s mining exports in the previous decade. Growth rates began slowing in 2017 and the return to “normal” investment levels has now taken place.

According to the latest construction figures published by the ABS, total construction in the June quarter increased by 0.4%. The result was less than the 1.0% increase which had been generally expected as well as the March quarter’s 3.8% increase after revisions. On an annual basis, the growth rate accelerated from 7.3% to 9.3%.

“In short, growth in construction work done waned in the June quarter, albeit after a stronger March quarter result,” said ANZ senior economist Adelaide Timbrell.

The figures came out on the same day as the latest home approvals and Commonwealth Government bond yields mostly fell moderately. By the close of business, the 3-year ACGB yield had lost 4bps to 3.78%, the 10-year yield had fallen 3bps to 4.07% while the 20-year yield finished 1bp lower at 4.42%.

In the cash futures market, expectations regarding further rate rises eased. At the end of the day, contracts implied the cash rate would barely change from the current rate of 4.07% and average 4.07% in September and 4.095% in October. February 2024 contracts implied a 4.175% average cash rate, as did May 2024 contracts, 11bps more than the current rate.

“The medium-term theme is that the capital stock needs to expand to meet the requirements of a growing population,” observed Westpac senior economist Andrew Hanlan. “Overlaid on that, the pandemic delayed the start of some projects and delayed the work on some projects. Current strength in work is in part due to those earlier delays, with many of the disruptions having eased.” He also noted new dwelling work is being supported by a backlog while renovation work “continues to deflate.”

Residential building construction expenditures were essentially flat, slightly higher than the 0.1% decline in the March quarter after revisions. On an annual basis, expenditure in this segment was 2.7% higher than the June 2022 quarter, up from the March quarter’s comparable figure of -3.4%.

Non-residential building spending increased by 0.6%, down from the previous quarter’s 4.2% increase. On an annual basis, expenditures were 6.7% higher than the June 2022 quarter, whereas the March quarter’s comparable figure was 6.2% after revisions.

Engineering construction increased by 0.7% in the quarter, a considerably smaller increase than the 6.5% rise in the March quarter. On an annual basis, spending in this segment was 15.5% higher than the June 2022 quarter, down from the March quarter’s comparable figure of 16.4% after revisions.

Quarterly construction data compiled and released by the ABS are not considered to be of a “primary” nature, unlike unemployment (Labour Force) and inflation (CPI) figures. However, the figures are viewed by economists and analysts with interest as they directly feed into quarterly GDP figures.