Summary: Construction spending up 0.1%, less than expected; up 1.2% from June 2023 quarter; Westpac: construction project pipeline received significant boost from latest government budgets; ACGB yields increase; rate-cut expectations soften; Westpac: sector faces difficulties from skilled labour shortages, elevated material costs; residential sector down 0.1%, non-residential building down 0.5%, engineering up 1.5%.

Construction expenditure increased substantially in Australia in the early part of last decade following a more-steady expansion through the 2000s. A large portion of the increase came from the commissioning of new projects and the expansion of existing ones to exploit a tripling in price of Australia’s mining exports in the previous decade.

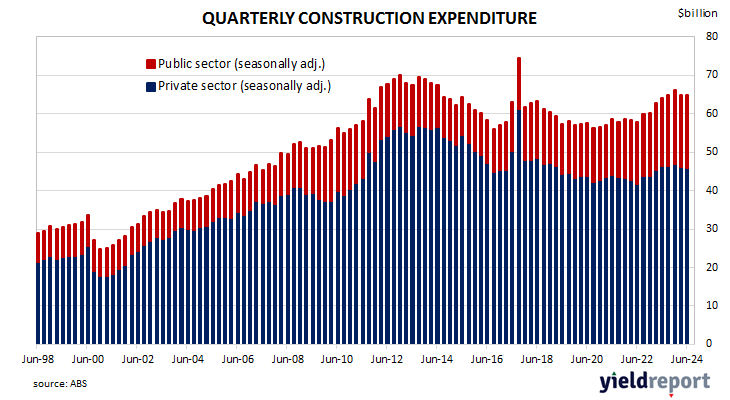

According to the latest construction figures published by the ABS, total construction in the June quarter increased by 0.1% on a seasonally adjusted basis. The result was less than the 0.5% increase which had been generally expected but in contrast with the March quarter’s 2.0% fall after revisions. On an annual basis, the growth rate slowed from 3.1% to 1.2%.

“The breakdown by construction type and sector remains consistent with the broader dynamics currently at play within the sector,” said Westpac senior economist Ryan Wells. “Of note, the construction project pipeline received a significant boost from the latest Federal and State Government budgets, particularly with respect to infrastructure funding, providing a support to current and future activity.”

The figures came out at the same time as July CPI numbers and domestic Treasury bond yields rose across a slightly flatter curve on the day. By the close of business, the 3-year ACGB yield had increased by 4bps to 3.53% while 10-year and 20-year yields both finished 2bps higher at 3.94% and 4.33% respectively.

Expectations regarding rate cuts in the next twelve months softened, although a February 2025 rate cut is still fully priced in. Cash futures contracts implied an average of 4.33% in September, 4.315% in October and 4.26% in November. February 2025 contracts implied 4.055% while July 2025 contracts implied 3.535%, 80bps less than the current cash rate.

“At the same time, the sector continues to face difficulties surrounding skilled labour shortages, elevated material costs and a fierce competition for resources,” Wells added. “This has largely presented as a slowdown in private residential construction that has crystallised over the past year, although other segments of private works, non-residential and infrastructure, have also slowed notably over the past six months.”

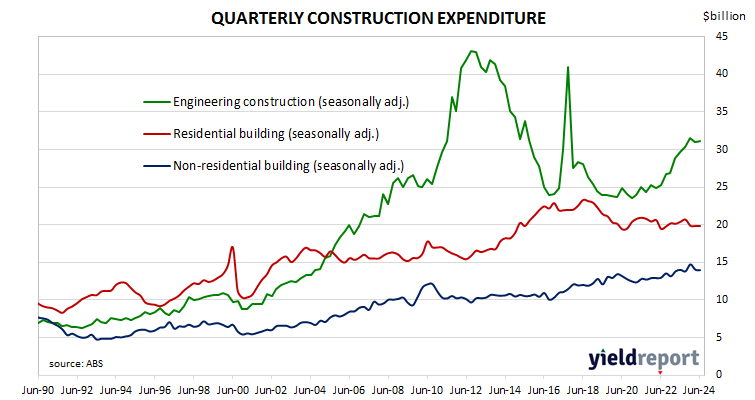

Residential building construction expenditures decreased by 0.1%, in line with the March quarter decline after revisions. On an annual basis, expenditure in this segment was 2.9% lower than the June 2023 quarter, down from the March quarter’s 1.4% decrease.

Non-residential building spending decreased by 0.5%, up from the previous quarter’s 4.7% fall. On an annual basis, expenditures were 0.3% lower than the June 2023 quarter, whereas the March quarter’s comparable figure was +1.5% after revisions.

Engineering construction increased by 1.5% in the quarter, in contrast with the 1.8% fall in the previous quarter. Spending on an annual basis in this segment was 4.8% higher than the June 2023 quarter, down from the March quarter’s comparable figure of 7.1% after revisions.

Quarterly construction data compiled and released by the ABS are not considered to be of a “primary” nature, unlike unemployment (Labour Force) and inflation (CPI) figures. However, the figures are viewed by economists and analysts with interest as they directly feed into quarterly GDP figures which are next due in early September.