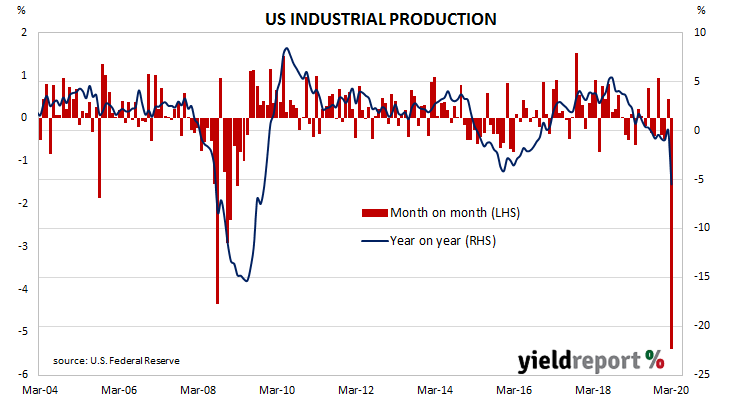

The Federal Reserve’s industrial production (IP) index measures real output from manufacturing, mining, electricity and gas company facilities located in the United States. These sectors are thought to be sensitive to consumer demand and so some leading indicators of GDP use industrial production figures as a component. Figures from early-2020 had been suggestive of a possible end to a downtrend which began in late-2018 but such hopes are now fanciful.

According to March figures, US industrial production contracted by 5.4%, worse than the +4.1% decrease which had been expected and a large turnaround from February’s revised figure of +0.5%. On an annual basis, the growth rate slowed from February’s figure of 0.00% to -5.5%.

ANZ economist Daniel Been noted the month’s fall was the “largest fall since 1946…Motor vehicle production slumped 28% due to both supply chain disruptions and reduced demand.” The report came on the same day as March’s retail sales figures were released and bond yields fell significantly at the long end. By the close of trade, the 2-year Treasury yield had added 2bps to 0.23%, the 10-year had lost 11bps to 0.64% and the 30-year yield finished 13bps lower at 1.27%.

The report came on the same day as March’s retail sales figures were released and bond yields fell significantly at the long end. By the close of trade, the 2-year Treasury yield had added 2bps to 0.23%, the 10-year had lost 11bps to 0.64% and the 30-year yield finished 13bps lower at 1.27%.