Last week, ANZ announced it would be offering to buy back its ANZ CPS 3 hybrids (ASX code: ANZPC) and issuing around $1 billion worth of ANZ Capital Notes 5 (ASX code: ANZPH). ANZ has now announced the margin above BBSW for distribution payments on the new capital notes.

As has been the usual practice in recent years, the margin has been set at the lower bound of the range. The indicative range was 3.80%-4.00% and hence the margin was set at 3.80%. When this margin is added to the current 3 month bank bill swap rate (BBSW) of 1.705%, investors can expect around 5.50% (annualised) for the first quarter and thereafter if BBSW rates do not alter materially. BBSW is typically at a fairly small margin to the RBA’s official cash rate which is currently 1.50%.

$552 million of the $1 billion offer has already been allocated to CPS 3 (ASX code: ANZPC) holders who are clients of syndicate brokers. Eligible CPS holders and other eligible ANZ security holders will have the next bite at the new capital notes. ANZ stated the final size of the offer will be determined after the ANZ Security-holder offer closes. If allocations reach $1 billion at this point, ANZ will close the offer and not proceed with the broker firm offer.

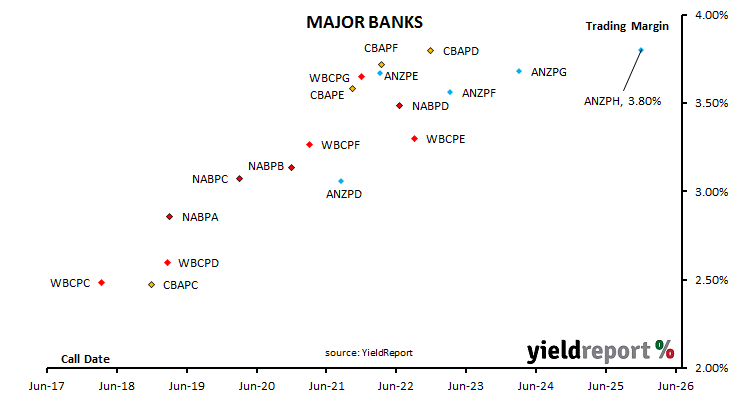

The chart below shows the trading margins of existing notes and bonds which are already listed on the ASX. In very simplified terms, a security’s trading margin is the sum of its annualised distributions as percentage of its price less BBSW. (In practice, unrealised annual capital gains/losses and accrued distributions are also taken into account.)

As at the close of business 23 August 2017.