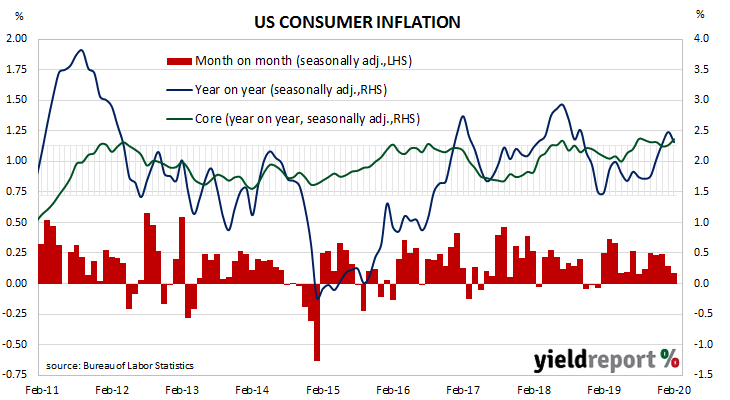

The annual rate of US consumer inflation halved from nearly 3% in the period from July 2018 to February 2019. It then fluctuated in a range from 1.5% to 2.0% through 2019 before rising above 2.0% in the final months of that year. “Headline” inflation is known to be volatile and so references are often made to “core” inflation for analytical purposes. This measure has mostly ranged between 1.7% and 2.3% in recent years.

The latest consumer price index (CPI) figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased by +0.1% on average in February, more than the flat result which had been expected and the same as January’s +0.1%. However, on a 12-month basis, the inflation rate slowed from January’s annual rate of 2.5% to 2.3%.

Core inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased on a seasonally-adjusted basis by +0.2% for the month, in line with expectations and the same as January’s increase. The annual rate ticked up from January’s 2.3% to 2.4% in February.

ANZ FX strategist John Bromhead said “The data were ignored by the market, which is focussed on the supply and demand shock the world is facing.” He noted “a potentially large deflationary shock hangs over us…” in contrast to the rising inflation rates of the past few months.

US Treasury bond yields mostly increased despite the “flight to safety” attitude present in equity markets. By the close of trade, the 2-year Treasury yield had slipped 1bp lower to 0.52% while the 10-year yield had increased by 8bps to 0.88% and the 30-year yield had gained 10bps to 1.39%.