Summary: Leading index declines in February; continues likelihood of above-trend growth; reading implies annual GDP growth to rise to around 5.5% during first half of 2021; RBA February GDP forecasts expected to be exceeded.

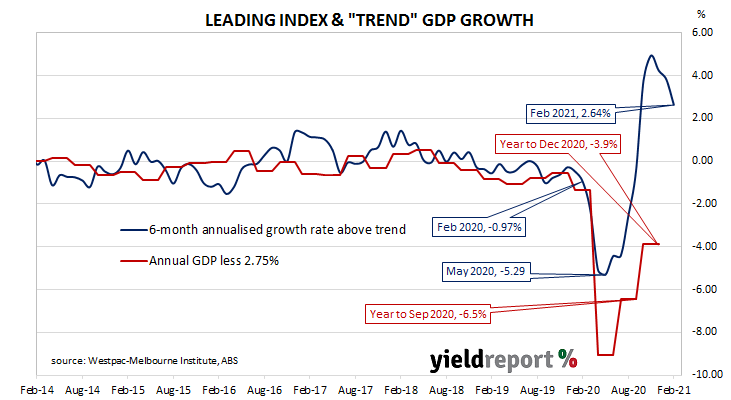

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic growth over the next three to six months. After reaching a peak in early 2018, the index trended lower through 2018 and 2019 before plunging to recessionary levels in the second quarter of 2020. Readings from the third and fourth quarters have been markedly higher.

The latest reading of the six month annualised growth rate of the indicator declined in February, from January’s revised figure of +3.83% to +2.64%.

Index figures represent rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum. The index is said to lead GDP by three to six months, so theoretically the current reading represents an annual GDP growth rate of around 5.5% in the second or third quarters of 2021.

Long-term Commonwealth Government bond yields moved moderately higher on the day, slightly outpacing rises in US Treasury bond markets overnight. By the end of the day, the 10-year ACGB yield had gained 3bps to 1.76% and the 20-year yield had increased by 4bps to 2.44%. The 3-year yield finished unchanged at 0.26%.

“From our perspective the key driver of growth in 2021 will be the household sector as a sharp fall in the currently elevated savings rate will free up considerable funds to support strong consumer spending,” said Westpac Chief Economist Bill Evans.

The RBA’s February Statement on Monetary Policy forecast GDP for the years ending June 2021 and December 2021 to be 8.0% and 3.5% respectively. Should the RBA’s forecasts prove to be accurate, an increase of just 1.3% across the March and June quarters is implied. Evans currently expects an increase of 1.6% in the March quarter alone.