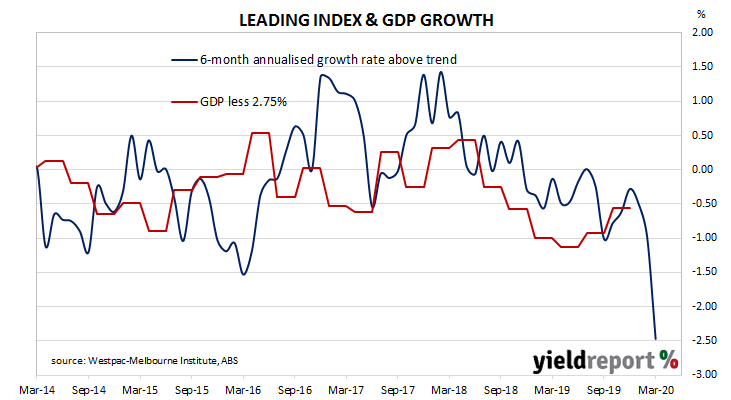

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic activity over the next three to six months. After reaching a peak in early 2018, the index trended lower through 2018, 2019 and the early months of 2020. In light of the mothballing of various sectors of the economy and restrictions on individuals’ movements, a sharp drop was expected in March.

The latest six months annualised growth rate of the indicator has fallen from February’s revised figure of –0.97% to -2.47% in March. After a brief improvement at the end of 2019, the index deteriorated in both January and February before the plunge in March.

Westpac chief economist Bill Evans said, “The sharply weaker signal is consistent with a deepening economic impact from the coronavirus pandemic. The Leading Index growth rate in March is the most negative seen since the Global Financial Crisis.”

Index figures represent rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum. The index is said to lead GDP by three to six months, so theoretically the current reading represents an annualised GDP growth rate of around 0.25% in the third quarter of 2020.

Commonwealth Government bond yields finished moderately lower, largely in line with falls in US markets overnight. By the end of the day, the 3-year ACGB yield had slipped 1bp to 0.25%, the 10-year yield had lost 2bps to 0.83% while the 20-year yield finished 4bps lower at 1.46%.