Summary: US leading index bounces; increase greater than expected; US in recession; “weak economic conditions” to persist.

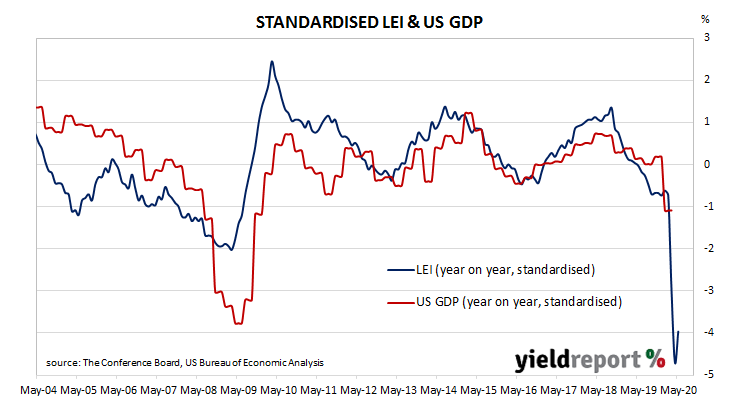

The Conference Board Leading Economic Index (LEI) is a composite index composed of ten sub-indices which are thought to be sensitive to changes in the US economy. The Conference Board describes it as an index which attempts to signal growth peaks and troughs; turning points in the index have historically occurred prior to changes in aggregate economic activity. Readings from March and April signalled “a deep US recession”.

The latest reading of the LEI indicates it rose by 2.8% in May. The result was better than the 2.2% increase which had been generally expected and it was a marked turnaround from April’s figure of -6.1% after it was revised down from -4.4%. On an annual basis, the LEI growth rate increased from April’s revised figure of -13.4% to -10.9%.

“The breadth and depth of the decline in the LEI between February and April suggest the economy at large will remain in recession territory in the near term,” said Ataman Ozyildirim, Senior Director of Economic Research at The Conference Board. While a “relative improvement” in unemployment claims was the main force behind the improvement, other factors such as new orders in manufacturing, consumers’ outlook and The Conference Board’s Leading Credit Index “still point to weak economic conditions.”

Changes over time can be large but once they are standardised, a clearer relationship with GDP emerges. The latest reading implies a year-on-year growth rate of around -2.0% in the December quarter.

US Treasury bond yields at the long end finished lower. By the end of the day, the 2-year bond yield remained unchanged at 0.19%, the 10-year yield had lost 2bps to 0.71% while the 30-year yield finished 5bps lower at 1.48%.