Summary: Leading index improves marginally in July; implies annual GDP growth to fall to ~-1.75% later this year/early next year; still consistent with recession; Westpac forecasts flat GDP in September quarter, 2.8% growth in December quarter; forecast based on easing of Victorian restrictions, no outbreaks elsewhere in Australia; RBA expects essentially no growth over second half of 2020.

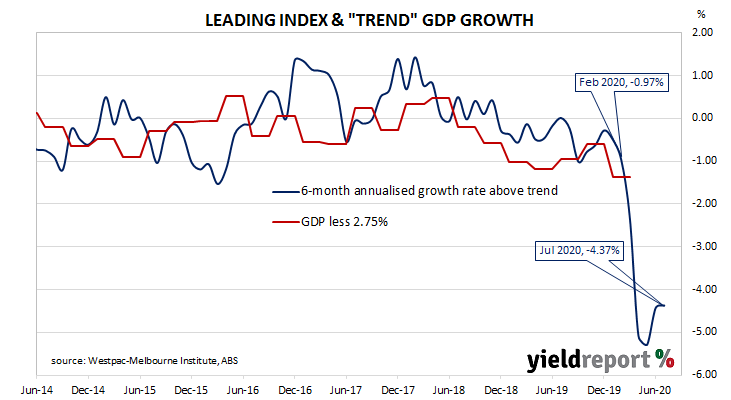

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic activity over the next three to six months. After reaching a peak in early 2018, the index trended lower through 2018, 2019 and the early months of 2020 before plunging to recessionary levels in the second quarter.

The latest reading of the six month annualised growth rate of the indicator increased ever-so-slightly, from June’s revised figure of –4.43% to -4.37% in July.

“The Index growth rate remains in deep negative territory consistent with recession,” Westpac chief economist Bill Evans.

Index figures represent rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum. The index is said to lead GDP by three to six months, so theoretically the current reading represents an annualised GDP growth rate of around -1.75% in the last quarter of 2020 and/or the first quarter of 2021.

Commonwealth Government bond yields remained stable except at the ultra-long end. By the end of the day, 3-year and 10-year ACGB yields both remained unchanged at 0.30% and 0.9% respectively while the 20-year yield finished 2bps lower at 1.44%.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.13%, continued to remain low. By the end of the day, contracts implied the cash rate would remain in a range of 0.125% to 0.135% through to the latter part of 2021.

Evans said Westpac now expects the Victorian economy to contract by 9%, offsetting growth elsewhere in Australia. “For Australia overall, we expect growth in the economy to be flat in the September quarter before lifting by 2.8% in the December quarter on the assumption that Victoria moves through Stage 4 to Stage 2 and the other states avoid ‘second wave’ outbreaks.”