Summary: Leading index improves in June; May index revised below April reading; implies annual GDP growth to fall to ~-1.75% later this year; still consistent with recession; “upside risk” to Westpac forecast of 7% contraction in June quarter; expects 3.5% growth in second half 2020.

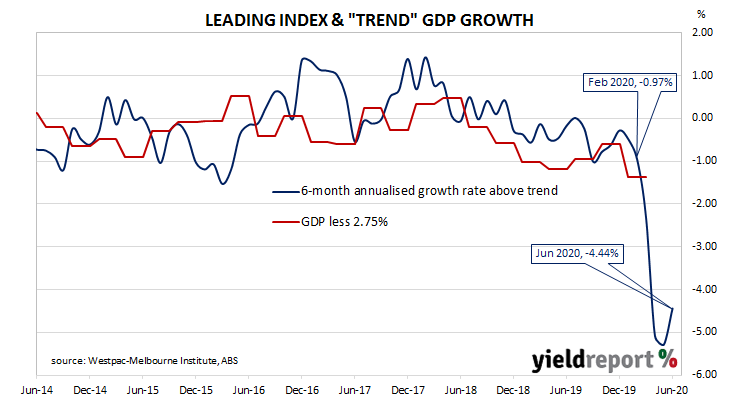

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic activity over the next three to six months. After reaching a peak in early 2018, the index trended lower through 2018, 2019 and the early months of 2020 before plunging to recessionary levels in the second quarter.

The latest reading of the six month annualised growth rate of the indicator increased from May’s revised figure of –5.29% to -4.44% in June.

After the previous month’s index was published, Westpac chief economist Bill Evans had described the Index’s growth rate as “consistent with an economic recession.” He repeated that statement in this latest release while noting the rise in hours worked in the June Labour Force figures, describing it as “particularly encouraging”.

Index figures represent rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum. The index is said to lead GDP by three to six months, so theoretically the current reading represents an annualised GDP growth rate of around -1.75% in the latter part of 2020.

Long-term Commonwealth Government bond yields moved moderately higher. By the end of the day, the 3-year ACGB yield remained unchanged at 0.31%, the 10-year yield had increased by 3bps to 0.91% while the 20-year yield finished 2bps higher at 1.53%.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.13%, continued to remain low. By the end of the day, contracts implied the cash rate would remain in a range of 0.13% to 0.14% through to the latter part of 2021.