Summary: Bell Potter views Macquarie hybrid as representing value late last week; some price increase since then; expects margin to major bank hybrids to narrow; may have already run its race.

Bell Potter’s fixed interest desk has identified Macquarie Bank Capital Notes 2 (ASX code: MBLPC) as an ASX-listed hybrid which represents value relative to other hybrid securities.

The hybrids have an issue margin of 4.70%, inclusive of franking credits. The distributions have been 40% franked to date, so Bell Potter expects just over $4.00 in cash over the next twelve months. The hybrids have a first call date on 22 December, 2025.

The report was put together late last week, with the price of MBLPC finishing at $107.50 on Friday 29 January. By the close of business on 3 February, the price had increased to $108.20, providing a 3.85% (40% franked) running yield and a trading margin of 2.78% over 3 month BBSW.

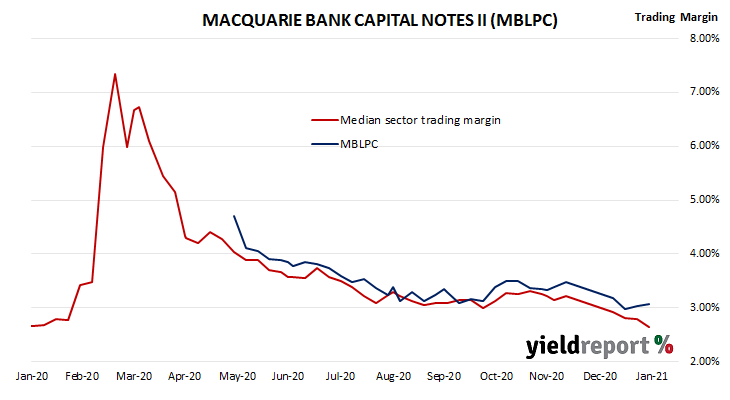

The Bell Potter team see the “trading margin differential narrowing between Macquarie and the major bank hybrids”. Since the Macquarie hybrid began trading in early June, the spread between MBLPC and a basket of major bank hybrids (ANZPH, CBAPG, WBCPH) with similar call dates has averaged 17bps (0.17%). At a trading margin of 278bps, the MBLPC are just 8bps higher to the average of these bank hybrids. It may be that the MBLPC’s have already run their race.