Summary: Private capital expenditures up 1.0% in March; slightly above expected figure; up 5.5% on annual basis; Westpac: machinery & equipment meets expectations, buildings & structures softer than anticipated; ACGB yields up; cash rate expectations largely unchanged; Westpac: business investment helping ease capacity constraints in some sectors; 2023/24 capex estimate 2.5% higher than previous estimate, 11.0% higher than comparable estimate from 2022/23; ANZ: suggests moderate growth in business investment this financial year.

Australia’s private capital expenditure (capex) spiked early in the 2010s on the back of investment in the mining sector. As projects were completed, capex growth rates fell away and generally remained negative for a good part of a decade. Capex as a percentage of GDP is now back to a level more in line with the long-term average.

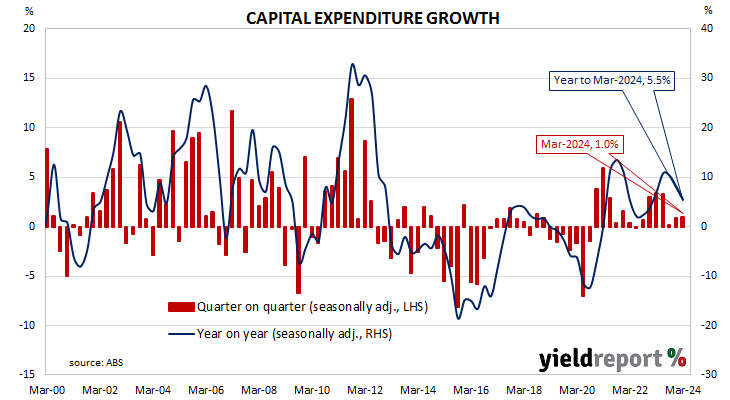

According to the latest ABS figures, seasonally-adjusted private sector capex in the March quarter increased by 1.0%. The result was slightly above the 0.7% increase which had been generally expected as well as the December quarter’s revised figure of 0.9%. On a year-on-year basis, total capex increased by 5.5%, down from 8.1% in the previous quarter after revisions.

“While machinery and equipment met our expectations, buildings and structures was softer than we anticipated,” said Westpac senior economist Pat Bustamante. “Non-mining capex grew 3.3% in the quarter, well above the pre- pandemic average quarterly growth of around 0.5%. This was partly offset by a 4.7% fall in mining capex.”

Short-term Commonwealth Government bond yields moved a touch higher on the day while longer-term yields moved up moderately. By the close of business, the 3-year ACGB yield had crept up 1bp to 4.08% while 10-year and 20-year yields both finished 4bps higher at 4.45% and 4.75% respectively.

In the cash futures market, expectations regarding rate cuts in the next twelve months remained largely unchanged. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.315% through June and 4.35% in August. November contracts implied 4.375%, February 2025 contracts implied 4.335% while May 2025 contracts implied 4.24%, 8bps less than the current cash rate.

“Businesses, who had to put investment spending on hold in the pandemic and struggled once again to expand capacity during various post-COVID supply shocks, still see a need to build their capital stocks,” said Westpac senior economist Pat Bustamante. “This is helping ease capacity constraints in some sectors, where reported capacity utilisation levels remain above average.”

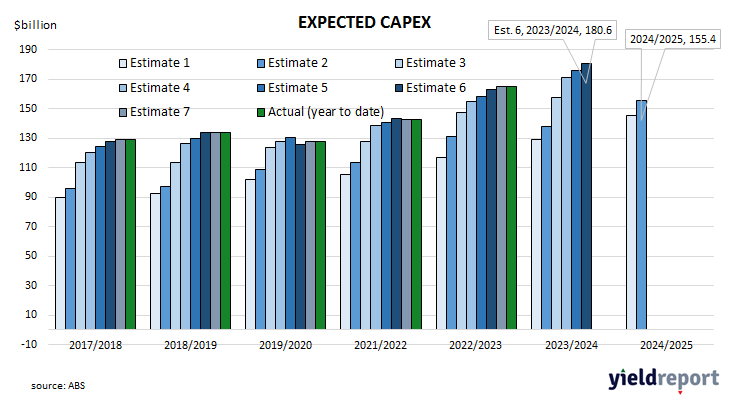

The report also contains capex estimates for the current financial year. The latest capex estimate for the 2023/24 financial year, Estimate 6, is $180.6 billion, 2.5% higher than February’s Estimate 5 and 11.0% higher than Estimate 6 of the 2022/23 financial year.

“These data are in nominal terms, so a reasonable part of nominal growth will be deflated away by increases in capital goods prices and construction costs,” said ANZ senior economist Blair Chapman. “Still, it suggests moderate growth in business investment this financial year.”