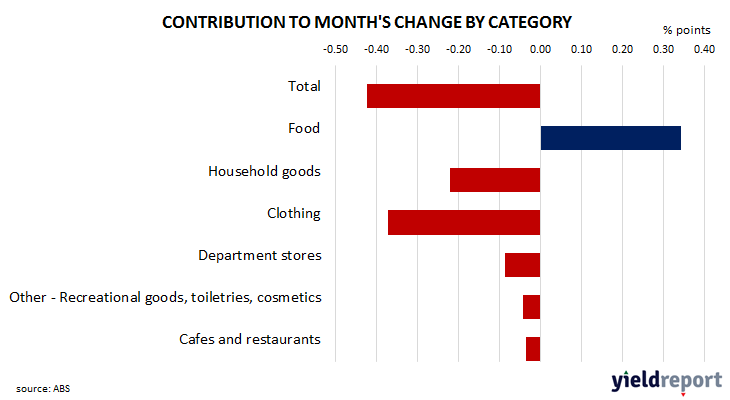

Summary: Retail sales down 0.4% in March, contrasts with expected gain; up 0.8% on 12-month basis; Westpac: another soft update, consumer environment remains flat at best; ACGB yields fall; rate-change expectations somewhat mixed; ANZ: highlights current pressures facing retail sector as households limit spending in response to cost of living pressures; largest influence on result from clothing, food sales.

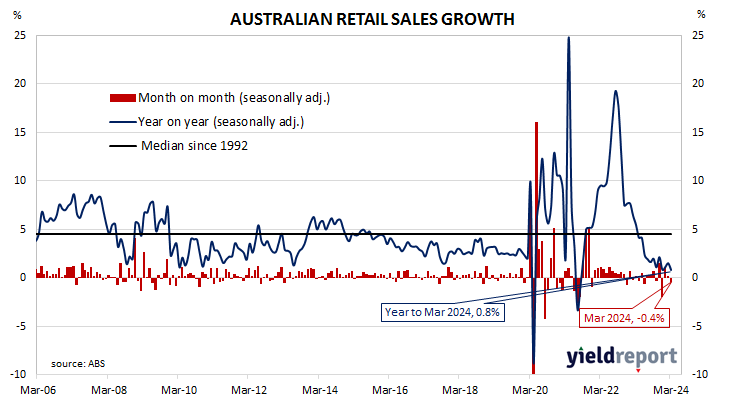

Growth figures of domestic retail sales spent most of the 2010s at levels below the post-1992 average. While economic conditions had been generally favourable, wage growth and inflation rates were low. Expenditures on goods then jumped in the early stages of 2020 as government restrictions severely altered households’ spending habits. Households mostly reverted to their usual patterns as restrictions eased in the latter part of 2020 and throughout 2021.

According to the latest ABS figures, total retail sales fell by 0.4% on a seasonally adjusted basis in March. The fall contrasted with the 0.2% increase which had been generally expected as well as February’s 0.2% gain after it was revised down from 0.3%. Sales increased by 0.8% on an annual basis, down from 1.5% after revisions.

“Overall, this was another soft update indicating the consumer environment remains flat at best,” said Westpac senior economist Matthew Hassan. “Our recently released Westpac Card Tracker report suggests April has been on the weak side as well. All of these flat aggregate results imply a continued contraction in per capita terms.”

Commonwealth Government bond yields fell almost uniformly across the curve, outpacing the falls of US Treasury yields on Monday night. By the close of business, the 3-year ACGB yield had lost 7bps to 4.03%, the 10-year yield had shed 6bps to 4.44% while the 20-year yield finished 7bps lower at 4.70%.

In the cash futures market, expectations regarding rate changes later this year or in 2025 were somewhat mixed. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.33% through May and 4.35% in June. However, November contracts implied a 4.40% average cash rate, February contracts implied 4.31%, while May 2025 contracts implied 4.22%, 10bps less than the current rate.

“This highlights the current pressures facing the retail sector as households limit spending in response to cost of living pressures,” said ANZ economist Madeline Dunk. “We think retail sales growth will pick up later in the year as consumer confidence improves and disposable incomes get a boost from the Stage 3 tax cuts.”

Retail sales are typically segmented into six categories (see below), with the “Food” segment accounting for 40% of total sales. However, the largest influences on the month’s total came from the “Clothing” segment where sales fell by 4.3%. “Food” sales had nearly as large an effect after sales rose by 0.9%.