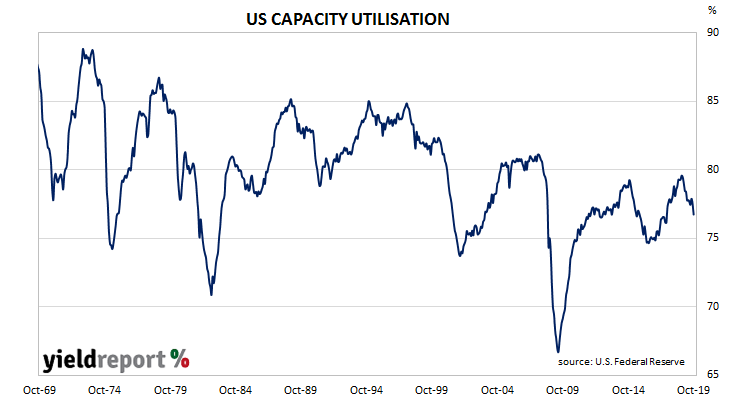

The Federal Reserve’s industrial production (IP) index measures real output from manufacturing, mining, electricity and gas company facilities located in the United States. These sectors are thought to be sensitive to consumer demand and so some leading indicators of GDP use industrial production figures as a component. A month ago, IP figures had suggested some chance of an end to a recent run of months in which US production has gone backwards. Figures from the latest report indicated that view was probably premature.

According to the latest figures released by the Fed, US industrial production dropped by 0.8% in October, less than the 0.3% fall which had been expected and more than double September’s 0.3% fall. On an annual basis, growth in industrial production went further into reverse from September’s rate of -0.1% to -1.1%.

ANZ economist Adelaide Timbrell said, “The GM strike is evident in the data, but the decline was not limited to that auto sector alone. Ex-vehicle and parts-manufacturing production was down 0.2%.”

Treasury bond yields barely moved on the day, perhaps supported by October’s retail sales figures which were also published. By the close of business, the 2-year US Treasury yield remained unchanged at 1.61%, the 10-year rate had crept up 1bp to 1.83% and the 30-year yield remained unchanged at 2.31%.

The reaction in the market for federal funds futures was not quite as restrained but it was not dramatic, either. The implied probability of a 25bps rate cut at the FOMC’s December meeting fell from 4% to zero while the likelihood of a January cut fell from 19% to 13%.