Summary: Home approval numbers up 5.5%% in May, more than expected; 8.5% lower than May 2023; Westpac: still bumping around decade lows; ACGB yields rise modestly; rate-rise expectations firm; ANZ: may see more modest growth in unit approvals in next month or two; house approvals up 1.3%, apartments up 14.2%; non-residential approvals down 0.9% in dollar terms, residential alterations down 6.2%.

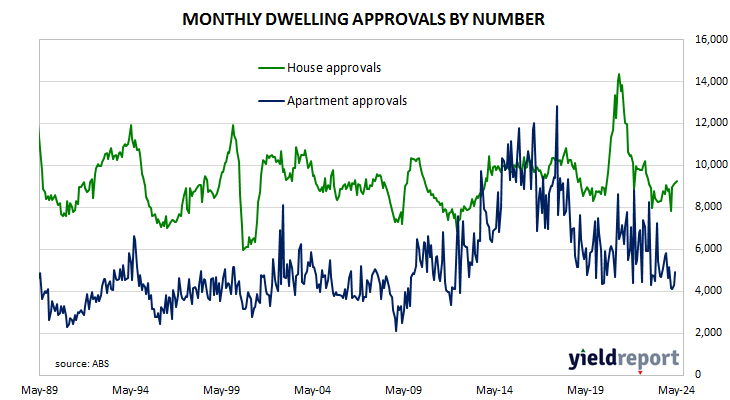

Building approvals for dwellings, that is apartments and houses, headed south after mid-2018. As an indicator of investor confidence, falling approvals had presented a worrying signal, not just for the building sector but for the overall economy. However, approval figures from late-2019 and the early months of 2020 painted a picture of a recovery taking place, even as late as April of that year. Subsequent months’ figures then trended sharply upwards before falling back through 2021, 2022 and 2023.

The Australian Bureau of Statistics has released the latest figures for May and they show total residential approvals increased by 5.5% over the month on a seasonally-adjusted basis. The rise was greater than the 1.7% gain which had been generally expected as well as April’s 1.9% rise after revisions. However, total approvals fell by 8.5% on an annual basis, a turnaround from the previous month’s revised figure of +5.1%. Monthly growth rates are often volatile.

“Despite this (exceeding expectations), approvals are still bumping around decade lows, stuck in the range that has prevailed since early 2023,” said Westpac senior economist Matthew Hassan. “And to the extent that there are more promising signs around detached houses, at least some of this looks to be a temporary pull forward effect associated with state government regulatory changes.

The figures were released on the same day as the latest retail sales number and Commonwealth Government bond yields moved modestly higher on the day, in contrast with the falls of US yields on Tuesday night. By the close of business, 3-year, 10-year and 20-year ACGB yields had all added 2bps to 4.13%, 4.44% and 4.76% respectively.

Expectations regarding rate rises in the next twelve months firmed slightly by the end of the day. In the cash futures market, contracts implied the cash rate has some chance of rising above the current rate of 4.32% in the short-term, with an average of 4.40% in August and 4.47% in November. February 2025 contracts implied 4.455% while May 2025 contracts implied 4.37%, 5bps above the current cash rate.

“Unit approvals also spiked in May last year, suggesting we may see more modest growth in unit approvals in the next month or two,” said ANZ economist Madeline Dunk.

Approvals for new houses increased by 1.3% over the month, up from April’s 0.5% rise after revisions. On a 12-month basis, house approvals were 12.1% higher than they were in May 2023, up from the previous month’s comparable figure of 10.1%.

Apartment approval figures are usually a lot more volatile and May approvals for this category rose by 14.2% after a 5.1% rise in April. However, the 12-month growth rate went further into reverse, from April’s revised rate of -4.1% to -32.1%.

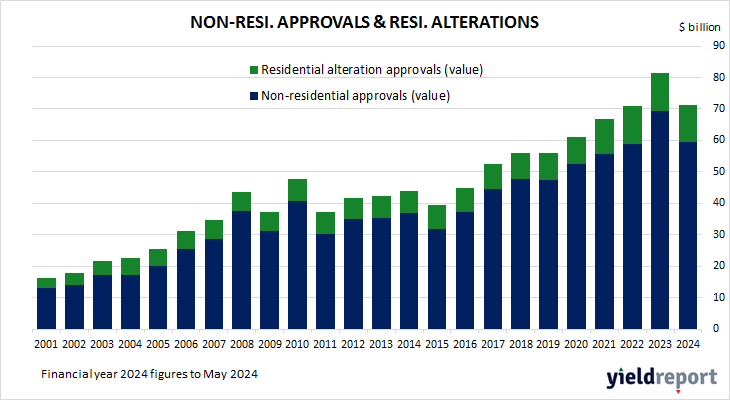

Non-residential approvals decreased by 0.9% in dollar terms over the month and were 16.3% lower on an annual basis. Figures in this segment also tend to be rather volatile.

Residential alteration approvals fell by 6.2% in dollar terms over the month but were still 5.1% higher than in May 2023.