The RBA’s quarterly Statement on Monetary Policy (SoMP) sets out the RBA’s view of domestic and international conditions. It also provides forecasts for Australian inflation and GDP growth based on the most recent data. While its view of international conditions will not move international markets, past SoMPs have moved Australian bond and currency markets from time to time.

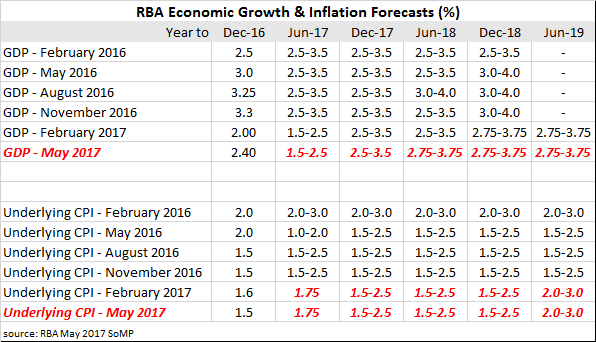

Expectations of anything dramatic coming out of the SoMP were low prior to its release. As Westpac’s currency team put it, “we would be surprised if the forecasts or messaging shifted valuations much, if at all.” On this occasion, there was little change in the statement. Inflation forecasts were left unchanged and there was only one modest shift in a GDP forecast; 0.25% was added to the forecast for the year to June 2018.

The SoMP was not entirely without controversy. ANZ’s David Planck picked on what appears to be some inconsistency in the RBA’s approach to inflation. “The point estimate for the year to June 2017 looks too low, for instance. Interestingly, the Bank’s forecasts for headline inflation don’t seem to line up with its commentary…The headline inflation numbers in its forecast table say otherwise.”

According to the RBA, “global economic conditions have picked up” and growth in Australia’s trading partners should be around “its long-run average this year before easing slightly in 2018.” Locally, things are looking positive, too. “Recent data are consistent with moderate growth in early 2017…Looking ahead, economic growth is expected to pick up gradually to be a bit above potential growth”. Underlying inflation is expected to be “around 2 per cent in early 2018” while headline inflation should be between 2% and 3% because of cigarette tax increases and price rises for utilities.