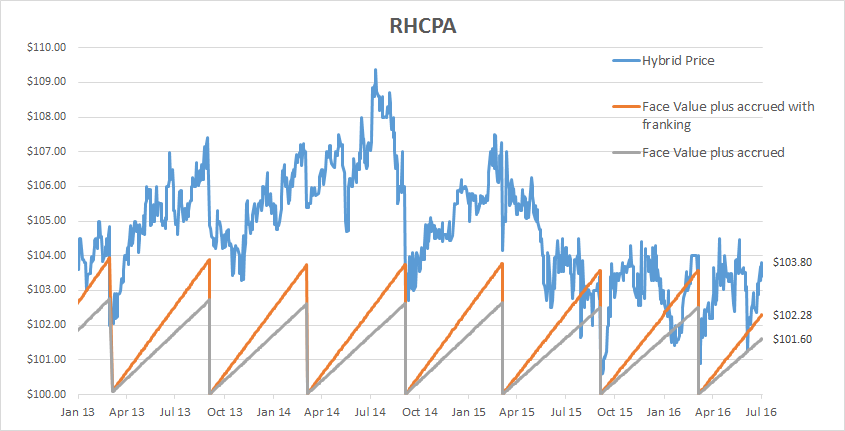

One of the traps for hybrids investors can fall into with any high yielding security which is past its call date is to buy it at more than its face value, only to have the issuer call it. Earlier this year Evans & Partners highlighted this issue. Using Ramsay Healthcare “CARES” (ASX code: RHCPA) as an example, E & P pointed out the way to avoid potentially-disappointing returns is to wait until the price is below the sum of the face value and the accrued income and that way if the securities are called the investor will not take a loss on the capital side.

It has been a little under six months since E &P last mentioned this issue but recently they decided to revisit this topic and once again, using the Ramsay Healthcare “CARES” as an example, they warn of this type of pitfall. From the chart above, readers will see the gap between the price of the CARES and the sum of the face value and accrued income has blown out (the orange line represents face value ($100) plus income plus franking credits while the grey line does not include franking credits). Readers will also notice how this is not unusual and, if not mindful of one’s timing, it would be all too easy to invest at a time which puts the investor at risk. That’s not to say there is a reason to expect the CARES to be called any time soon, it is just a risk investors should know about and seek to minimise, perhaps more so now as the gap has widened in recent times.