Barely more than a day after Peet announced it would be issuing a new series of ASX-listed notes, it has announced the margin on its new simple corporate bonds (ASX code: PPCHB). The company had initially sought to raise $50 million, but after Peet received additional demand for the bonds, the book-build was closed early. Even though Peet received offers in excess of $50 million, it decided to limit the amount raised and therefore there will be scaling back of applications.

Barely more than a day after Peet announced it would be issuing a new series of ASX-listed notes, it has announced the margin on its new simple corporate bonds (ASX code: PPCHB). The company had initially sought to raise $50 million, but after Peet received additional demand for the bonds, the book-build was closed early. Even though Peet received offers in excess of $50 million, it decided to limit the amount raised and therefore there will be scaling back of applications.

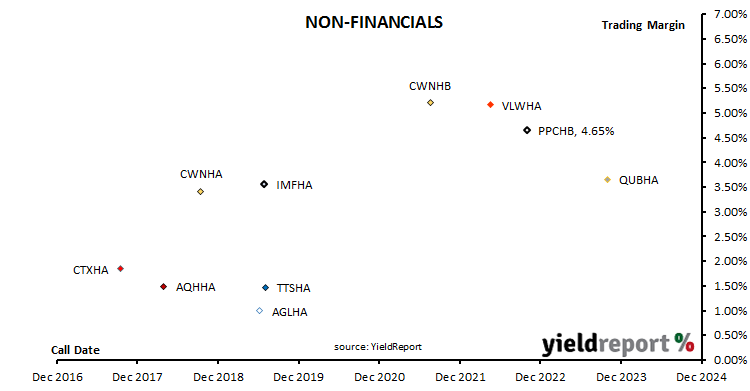

It has been some years since a margin was set not at the bottom of an issue’s indicative range and the margin on Peet’s new securities has stuck to this pattern. The indicative range was 4.65%-4.75% and hence the margin was set at 4.65%. When this margin is added to the current 3 month bank bill swap rate (BBSW) of 1.72%, investors can expect nearly 6.40% annualised for the first quarter and thereafter if BBSW rates do not alter materially. BBSW is typically at a fairly small margin to the RBA’s official cash rate which is currently 1.50%.

The chart below shows the trading margins of existing notes and bonds which are already listed on the ASX. In very simplified terms, a security’s trading margin is the sum of its annualised distributions as percentage of its price less BBSW. (In practice, unrealised annual capital gains/losses and accrued distributions are also taken into account.)

As at the close of business 22 June 2017.