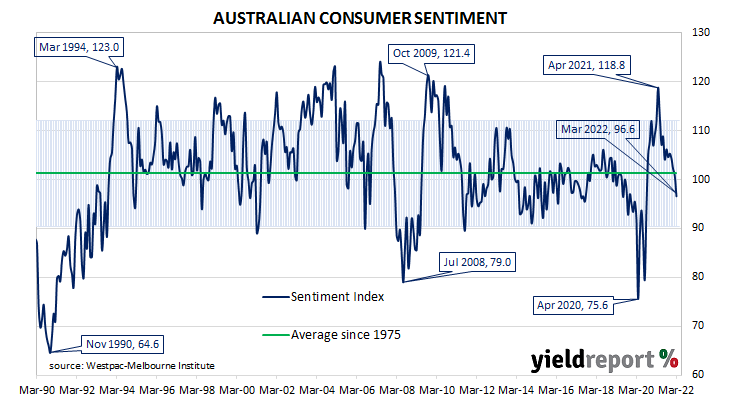

Summary: Household sentiment deteriorates in March; index fall “no surprise” given floods, inflation concerns, higher interest rates; all five sub-indices lower; conditions “supportive” due to strong balance sheets, excess savings, rising income growth; Unemployment Expectations index lower.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again in mid-July 2018. Both readings then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April 2020 but, after a few months of to-ing and fro-ing, it then staged a full recovery.

According to the latest Westpac-Melbourne Institute survey conducted in the first week of March, household sentiment has again deteriorated. Their Consumer Sentiment Index fell from February’s reading of 100.8 to 96.6 in March. The latest figure is now noticeably lower than the long-term average reading of just over 101.

“The latest monthly fall comes as no surprise. The war in Ukraine, the floods in south-east Queensland and northern New South Wales, ongoing concerns about inflation and higher interest rates were all likely to impact confidence, although the size of the decline is still notable,” said Westpac Chief Economist Bill Evans. Any reading of the Consumer Sentiment Index above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic.

Domestic Treasury bond yields increased on the day despite the report, following the lead of moderately higher US Treasury yields in overnight trading. By the close of business, 3-year and 10-year ACGB yields had both gained 8bps to 1.76% and 2.32% respectively while the 20-year yield finished 7bps lower at 2.78%.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.05%, firmed with respect to rate rises in the second half of 2022. At the end of the day, contract prices implied the cash rate would rise gradually from the current rate of 0.050% to 0.12% by May, then increase to 0.61% by August and then to 1.51% by February 2023.

“Overall, the consumer backdrop remains supportive with a strong balance sheet and excess savings, as well as rising income growth from a tight labour market and higher wage growth. The key question for the economy will be whether the consumer utilises this through spending, making the evolution of sentiment through the year a key indicator to watch,” said Morgan Stanley Australia equity strategist Chris Read. He currently expects domestic demand to be “solid” through 2022 even if household remain cautious.

All five sub-indices registered lower readings, with the “Economic conditions – next 12 months” sub-index posting the largest monthly percentage loss. The reading of the “Economic conditions next 5 years” sub-index also deteriorated noticeably.

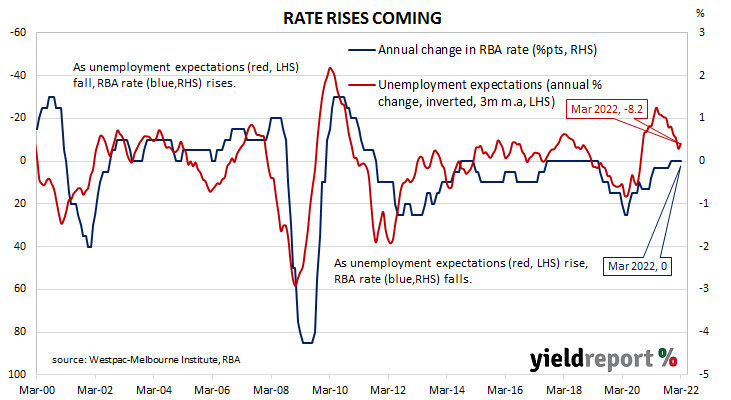

The Unemployment Expectations index, formerly a useful guide to RBA rate changes, fell from 102.8 to 101.8. Lower readings result from fewer respondents expecting a higher unemployment rate in the year ahead.