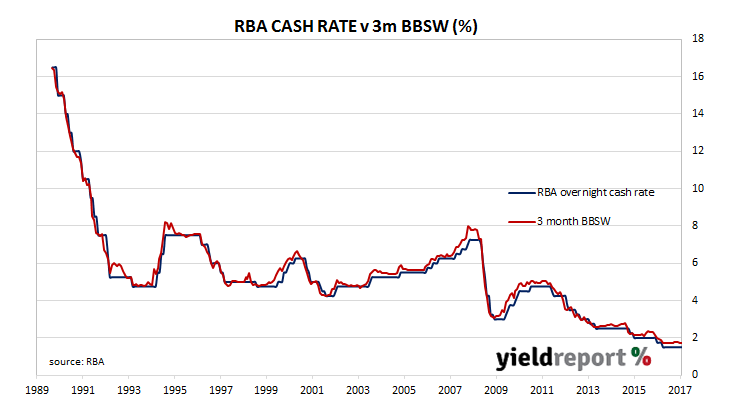

The June RBA meeting is not one of the four months of the year in which most rate changes have been historically made and for that reason alone no one expected anything to happen. Aside from this historical observation, the RBA has made it quite clear is concerned by the build-up of household debt. Even if it thought the economy was weak and need of monetary stimulus, interest rates are historically very low and a cut would be unlikely to aid business or household sectors much at all.

One of the main points to come from the statement which followed the meeting was the RBA Board still viewed housing market conditions as a concern. Another was the weakness in the first quarter is likely to prove temporary. Both of these issues is a tick for a higher interest rate. On the other hand, some economists think economic conditions may weaken in 2018 as consumer spending growth is constrained by low wage growth, which is a tick for lower interest rates.

Here’s what a few economists had to say.

Matthew Hassan, Westpac

“The structure of the statement is also worth noting. The most important concluding paragraph is completely unchanged, stating policy was unchanged and giving no forward guidance. The penultimate paragraph discusses housing market conditions, a key area of concern for the Bank according to its most recent minutes and the focus of its latest macro-prudential policy measures.

All up, we see no reason to change our current view that the official cash rate will remain on hold throughout 2017 and 2018.”

David Plank, ANZ thought the RBA may be wrong when it comes to first quarter weakness proving to be temporary. “We think there are good reasons to believe that the pace of economic growth may have stepped down in a sustained fashion.” If weakness in the first quarter continues he thinks core inflation will be unlikely to rise. “In which case, the Bank’s policy settings may be challenged.” In other words, there may be an incentive for the official rate to be lowered. Not yet, however. “On balance, we continue to see the RBA on hold for the foreseeable future. We do, however, think the Bank is underplaying the likely weakness in economic activity in the first half of 2017.”

Daniel Blake, Morgan Stanley

“We have the benefit of incorporating the most recent data and policy developments, with the next round of RBA forecasts not published until August 4th. But even still, we question whether policymakers are too optimistic on the quality of employment growth and the leverage that Australia has to improved global growth, while not factoring the risk that reported business conditions to soften alongside already weakening revenue/earnings trends…As a result, we hold our forecast for the RBA to leave the cash rate at 1.5% into 2019, although the risk of another round of cuts has increased and we would expect the Bank to respond quickly to any emerging recessionary labour market dynamics.”