Summary: Non-farm payrolls increase by 850K in June; more than expected; previous two months’ figures revised up by 15K; jobless rate up, participation rate steady; 40% of gain from leisure/hospitality; total employment still 6.8 million below February 2020; “nothing” for Fed to become hawkish about; jobs-to-population ratio steady at 58%; underutilisation rate falls below 10%; annual hourly pay growth increases to 3.6%.

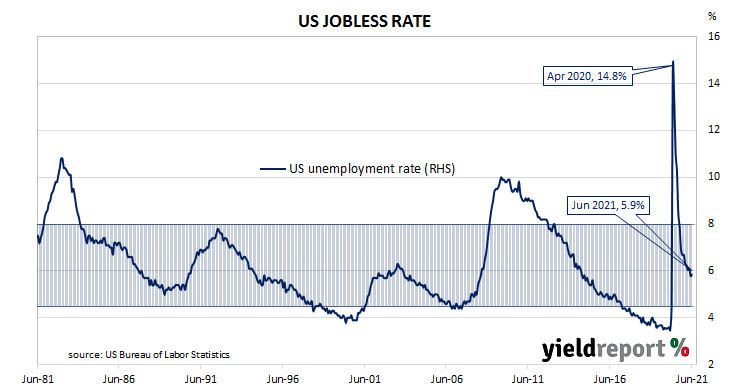

The US economy ceased producing jobs in net terms as infection controls began to be implemented in March 2020. The unemployment rate had been around 3.5% but that changed as job losses began to surge through March and April of 2020. The May 2020 non-farm employment report represented a turning point and subsequent months provided substantial employment gains. Changes in recent months have been generally more modest but still well above the long-term monthly average.

According to the US Bureau of Labor Statistics, the US economy created an additional 850,000 jobs in the non-farm sector in June. The increase was above the 700,000 which had been generally expected earlier in the week and greater than the 683,000 jobs which had been added in May after revisions. Employment figures for April and May were revised up by a total of 15,000.

The unemployment rate rose from May’s rate of 5.8% to 5.9%. The total number of unemployed increased by 168,000 to 9.484 million while the total number of people who are either employed or looking for work increased by 150,000 to 161.086 million. Despite a higher number of people in the labour force, the participation rate remained unchanged from May’s rate of 61.6%.

“While headline payrolls did beat expectations by a considerable way, the unemployment rate rose and 40% of jobs gains was led by the leisure and hospitality industry,” said NAB senior economist NAB Tapas Strickland.

US Treasury yields fell modestly on the day. By the close of business, the 2-year bond yield had lost 2bps to 0.24% while 10-year and 30-year yields each finished 3bps lower at 1.43% and 2.04% respectively.

“Overall the level of payrolls is still 6.8 million below pre-pandemic February 2020 levels and is still below the level of substantial progress needed by the Fed. As such there is nothing in this report for the Fed to become hawkish about,” Strickland concluded.