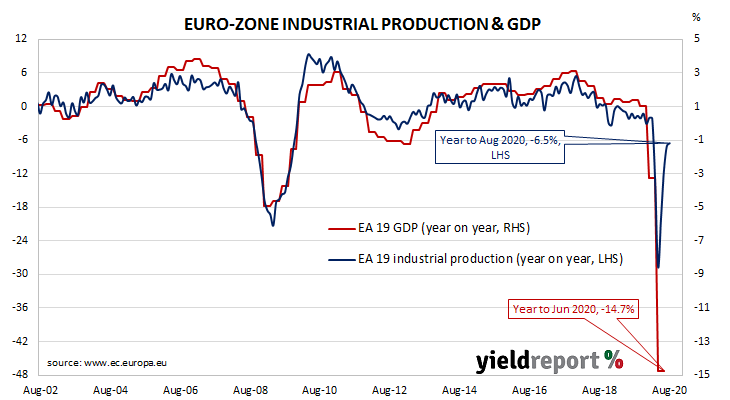

Summary: Euro-zone industrial production continues recovery after huge falls in March, April; monthly figure significantly more than consensus estimate; annual rate still very negative; German and Spanish production contract.

Following a recession in 2009/2010 and the debt-crisis of 2010-2012 which flowed from it, euro-zone industrial production recovered and then reached a peak four years later in early-2016. Growth rates then fell and recovered through 2016/2017 before beginning a steady and persistent slowdown from the start of 2018. That decline was transformed into a plunge in March and April. However, the months following have produced an almost-equally steep bounce.

According to the latest figures released by Eurostat, euro-zone industrial production expanded on a seasonally-adjusted basis by 0.7% in August. The increase was less than the 0.8% increase which had been generally expected and substantially less than July’s revised figure of 5.0%. On an annual basis, the seasonally-adjusted growth rate increased from July’s revised rate of -7.0% to -6.5%*.

German and French 10-year sovereign bond yields moved lower on the day. By the close of business, German and French 10-year yields had each shed 2bps to -0.58% and -0.31% respectively.

Industrial production growth proved to be patchy among the four largest euro-zone economies. Germany’s production contracted by 0.2% in August while the comparable figures for France, Spain and Italy were 1.3%, -0.2% and 7.7% respectively.

As with other countries’ measures of industrial production, Eurostat’s industrial production index measures the output and activity of industrial sectors in euro-zone countries on aggregate.

* Eurostat’s published annual growth figures are calculated using index figures which are “calendar adjusted”, not “seasonally adjusted”. The published Eurostat figure was -7.2%.