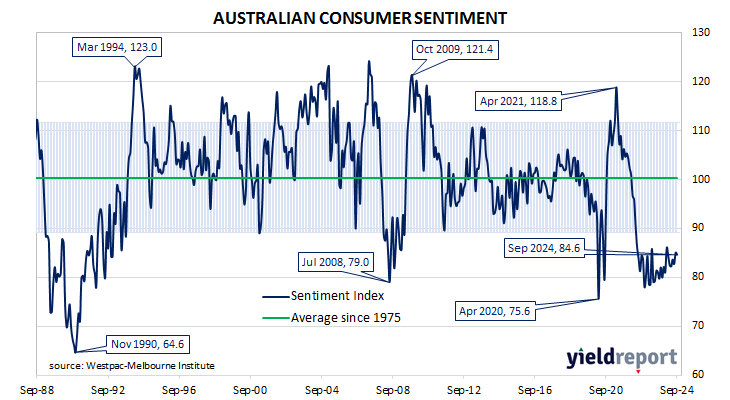

Summary: Westpac-Melbourne Institute consumer sentiment index slips in September; Westpac: pessimism over past two years showing no real signs of lifting; ACGB yields fall; rate-cut expectations firm, first cut fully priced in for February; Westpac: consumers becoming more concerned about where economy headed; three of five sub-indices fall; more respondents expecting higher jobless rate.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again in mid-July 2018. Both measures then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April 2020 but, after a few months of to-ing and fro-ing, it then staged a full recovery. However, consumer sentiment then weakened considerably and has languished at pessimistic levels since mid-2022 while business sentiment has been more robust.

According to the latest Westpac-Melbourne Institute survey conducted over the first four business days of September, household sentiment has remained largely unchanged at a quite pessimistic level. Their Consumer Sentiment Index slipped from August’s reading of 85.0 to 84.6, a reading which is significantly lower than the long-term average reading of just over 101 and below the “normal” range.

“The pessimism that has dominated for over two years now is still showing no real signs of lifting,” said Westpac senior economist Matthew Hassan.

Any reading of the Consumer Sentiment Index below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic.

The report came out the same morning as NAB’s latest business survey and domestic Treasury bond yields fell on the day, steepening the yield curve. By the close of business, the 3-year ACGB yield had lost 2bps to 3.52% while 10-year and 20-year yields both finished 5bps lower at3.92% and 4.33% respectively.

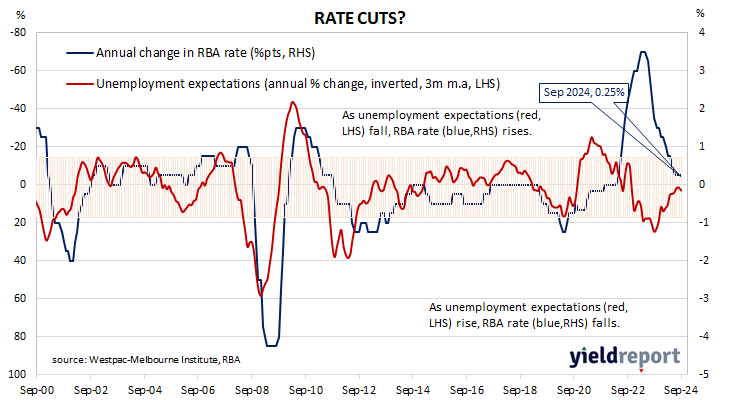

Expectations regarding rate cuts in the next twelve months firmed, with a February 2025 rate cut fully priced in. Cash futures contracts implied an average of 4.335% in September, 4.32% in October and 4.275% in November. February 2025 contracts implied 4.08% while August 2025 contracts implied 3.42%, 92bps less than the current cash rate.

“However, the focus does look to be shifting,” Hassan added. “While cost-of-living pressures are becoming a little less intense and fears of further interest rate rises have eased, consumers are becoming more concerned about where the economy may be headed and what this could mean for jobs.”

Three of the five sub-indices registered lower readings, with the “Economic conditions – next 12 months” sub-index posting the largest monthly percentage loss.

The Unemployment Expectations index, formerly a useful guide to RBA rate changes, rose from 133.5 to 138.4, noticeably above the long-term average of 129.1. Higher readings result from more respondents expecting a higher unemployment rate in the year ahead.