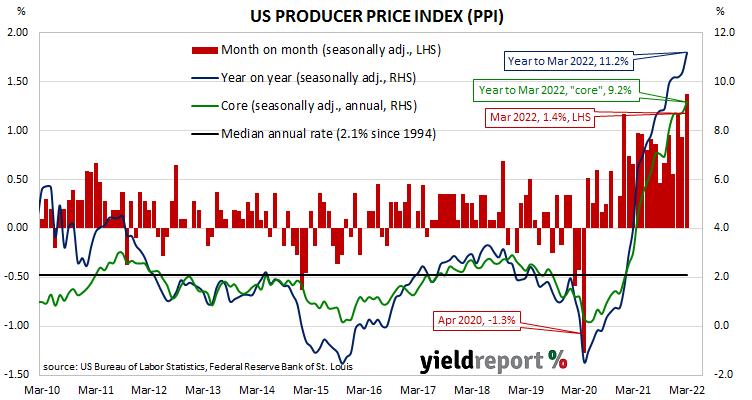

Summary: US producer price index (PPI) up 1.4% in March, larger than expected; annual rate rises from 10.4% to 11.2%; “core” PPI up 1.0%; “pipeline inflationary pressures remain elevated”; US Treasury yields lower, rate-rise expectations ease; factors behind figures unlikely to be resolved in short-term.

Around the end of 2018, the annual inflation rate of the US producer price index (PPI) began a downtrend which continued through 2019. Months in which producer prices increased suggested the trend may have been coming to an end, only for it to continue, culminating in a plunge in April 2020. Figures returned to “normal” towards the end of that year but recent months’ annual rates have been well above the long-term average.

The latest figures published by the Bureau of Labor Statistics indicate producer prices rose by 1.4% after seasonal adjustments in March. The increase was larger than the consensus expectation of 1.2% as well as February’s revised figure of 0.9%. On a 12-month basis, the rate of producer price inflation after seasonal adjustments accelerated from February’s revised rate of 10.4% to 11.2%.

Producer prices excluding foods and energy, or “core” PPI, rose by 1.0% after seasonal adjustments. The increase was double the 0.5% which had been generally expected and substantially greater than February’s revised figure of 0.4%. The annual rate increased from February’s revised rate of 8.8% to 9.2%.

“This suggests that, while yesterday’s core CPI inflation was a touch below expectations, pipeline inflationary pressures remain elevated,” said ANZ senior economist Catherine Birch.

US Treasury bond yields generally fell on the day, although ultra-long yields remained steady. By the close of business, 2-year and 10-year Treasury yields had both shed 4bps to 2.37% and 2.69% respectively while the 30-year yield finished unchanged at 2.81%.

In terms of US Fed policy, expectations for a higher federal funds rate over the next 12 months eased slightly. By the close of business, May contracts implied an effective federal funds rate of 0.75%, 42bps higher than the current spot rate. June contracts implied 1.035% while March 2023 futures contracts implied an effective federal funds rate of 2.63%, 230bps above the spot rate.

Birch said the likely factors behind the figures, a tight US jobs market, war in Ukraine and supply-chain bottlenecks, will probably not be resolved in the short-term. “That will keep pushing input costs higher, feeding CPI inflation and pressuring the Fed.”

The producer price index is a measure of prices received by producers for domestically produced goods, services and construction. It is put together in a fashion similar to the consumer price index (CPI) except it measures prices received from the producer’s perspective rather than from the perspective of a retailer or a consumer. It is another one of the various measures of inflation tracked by the US Fed, along with core personal consumption expenditure (PCE) price data.