Capital expenditure in the third quarter was weaker than the -2.9% expected and declined by 9.2% compared to the previous quarter. There were immediate movements in markets as a result of the figures as cash markets increased the odds of rate cuts next year, 10 year bond yields fell 3bps and the currency markets reacted by sending the Aussie dollar lower as it too factored in lower interest rates in the future.

Equipment spending fell by 8.2% and building/structure spending fell by 9.8%. By industry, the mining sector fell 10.4%, the services sector fell 9.2% while the manufacturing sector provided the one piece of good news and increased by 6.9%.

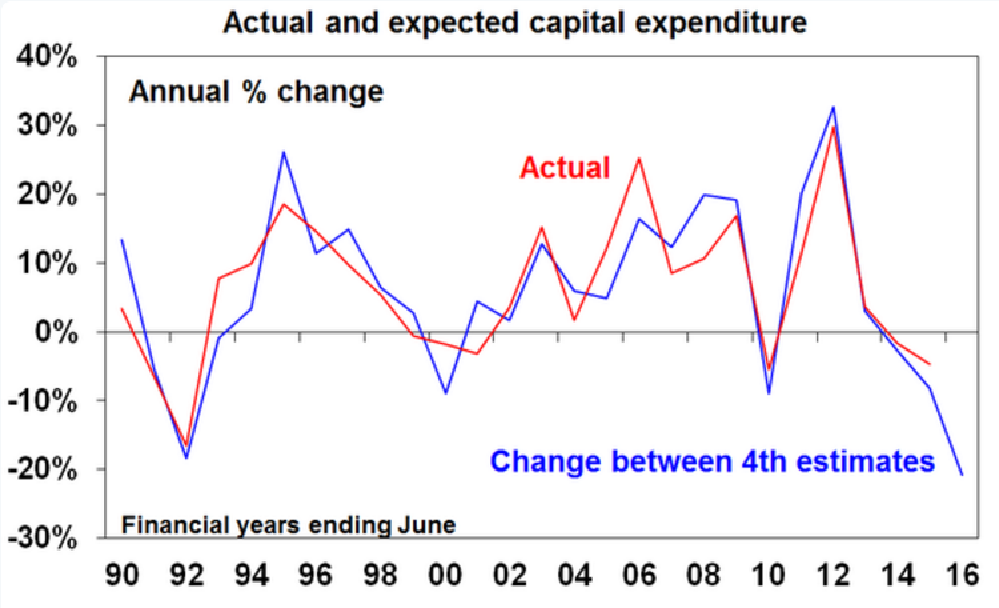

Estimate 4 for 2015/16 capex plans is now $120.4 billion, 4% higher than August’s Estimate 3 of $104 billion but 20.9% lower on the previous year’s Estimate 4 of $145 billion.

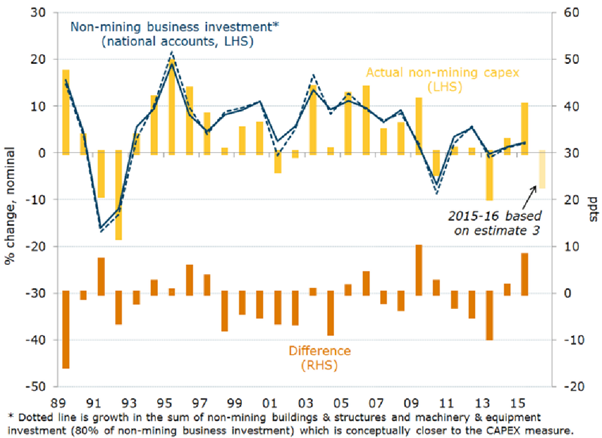

AMP’s chief economist Shane Oliver said the poor Q3 capex plans would partly offset the strong trade contribution to GDP growth. He said Q3 GDP would not be negative but it would not be as strong as some thought after the trade figures came out earlier in the week. Westpac said they had revised their Q3 GDP forecasts back to 0.7% and 2.1% for the 2015/2016 year. ANZ senior economist Justin Fabo pursued a slightly different angle and suggested the figures be treated with some caution as the chart below was “a reminder of just how poor a guide it is to actual non-mining investment.”