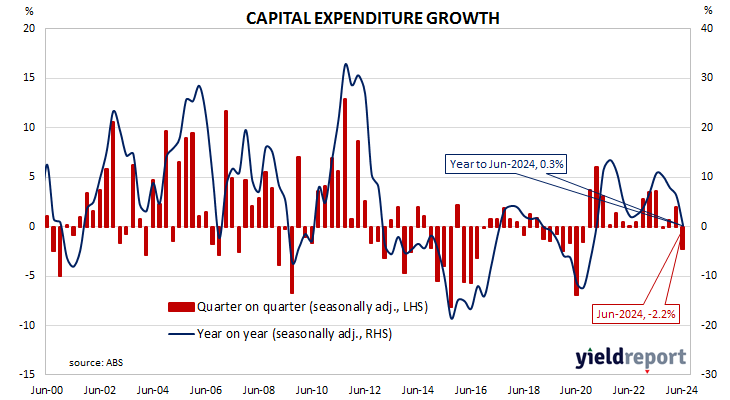

Summary: Private capital expenditures down 2.2% in June quarter; contrasts with expected rise; up 0.3% on annual basis; ANZ: growing divide between industries; ACGB yields up modestly; rate-cut expectations slightly softer; Westpac: growing divide between industries; 2023/24 capex estimate 0.5% higher than previous estimate, 10.2% higher than comparable estimate from 2022/23; Westpac: real capex spending could increase by ~3.25% in 2024/25.

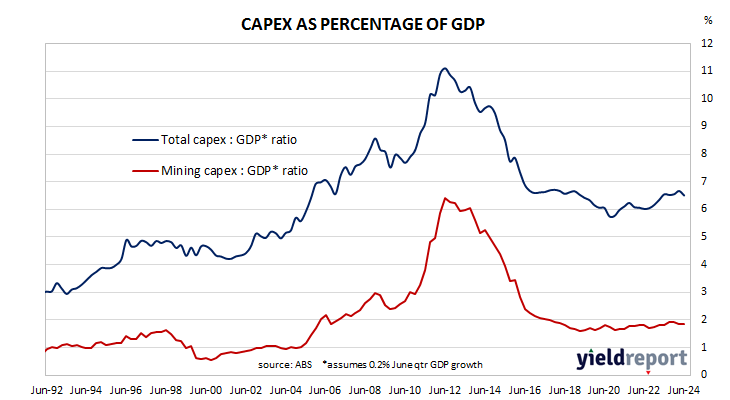

Australia’s private capital expenditure (capex) spiked early in the 2010s on the back of investment in the mining sector. As projects were completed, capex growth rates fell away and generally remained negative for a good part of a decade. Capex as a percentage of GDP is now back to a level more in line with the long-term average.

According to the latest ABS figures, seasonally-adjusted private sector capex fell by 2.2% in the June quarter. The result contrasted with the 1.0% increase which had been generally expected as well as the March quarter’s 1.9 rise. On a year-on-year basis, total capex increased by 0.3%, down from 6.3% in the previous quarter after revisions.

“The Q2 capex release showed softness in the quarter, but still points to a positive, but cooling, investment outlook,” said ANZ Head of Australian Economics Adam Boyton.

Commonwealth Government bond yields moved modestly higher on the day, largely in line with overnight movements of US Treasury yields. By the close of business, the 3-year ACGB yield had crept up 1bp to 3.54%, the 10-year yield had added 2bps to 3.96% while the 20-year yield finished 1bp higher at 4.34%.

Expectations regarding rate cuts in the next twelve months softened slightly, although a February 2025 rate cut is still fully priced in. Cash futures contracts implied an average of 4.33% in September, 4.315% in October and 4.265% in November. February 2025 contracts implied 4.07% while July 2025 contracts implied 3.535%, 80bps less than the current cash rate.

“While private business capex remains elevated, there is a growing divide between industries that are experiencing higher demand on the back of increased public spending and the population rebound, and those at the coal face of the consumer-led slowdown,” said Westpac senior economist Pat Bustamante.

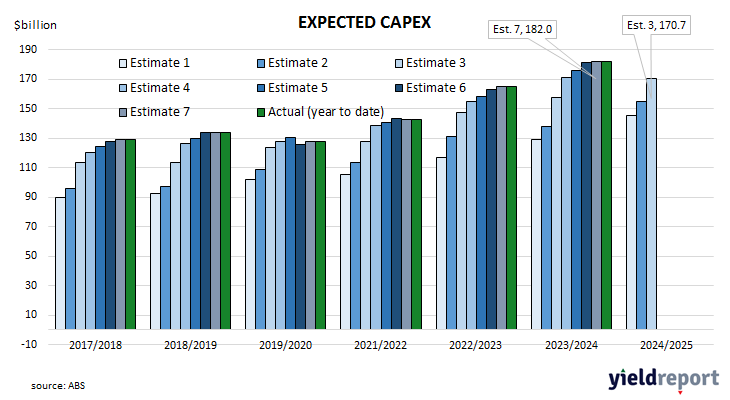

The report also contains capex estimates for the current financial year as well as the following financial year. The latest capex estimate for the 2023/24 financial year, Estimate 7, is $182.0 billion, 0.5% higher than May’s Estimate 6 and 10.2% higher than Estimate 7 of the 2022/23 financial year.

“Adjusting spending plans for prices suggests that real capex spending could increase by around 3.25% in 2024/25,” Bustamante added. “Spending plans suggests that real non-mining capex could grow by around 5.75% in 2024/25, while real mining capex could fall by around 2.75%. If realised, this will help ensure the non-mining sector adds to its capital stock.”