Summary: Private sector credit grows by 0.6% in September, above +0.5% expected; annual growth rate rises from 4.7% to 5.3%; “early signs” business investment may be lifting “meaningfully”; owner-occupier loans account for two-thirds of net growth; investor loans up modestly again, personal loans down again.

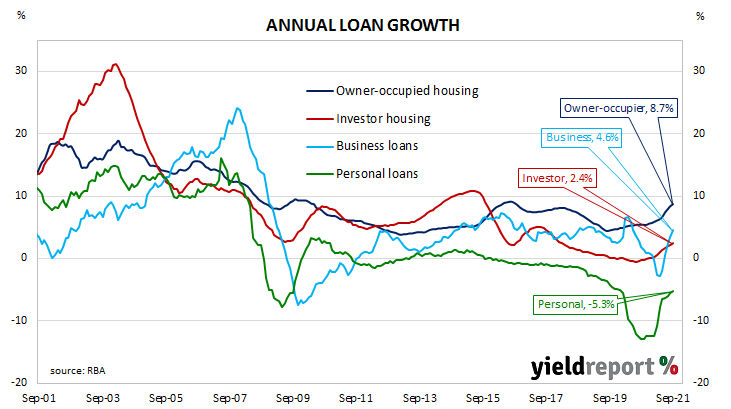

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since late-2015. Private sector credit growth appeared to have stabilised in the September quarter of 2018 only to deteriorate through to the end of 2019. The early months of 2020 provided some positive signs but they disappeared in April 2020. Recent months’ figures indicate the downtrend is over and annual growth rates are now back to levels last seen in 2016 and 2017.

According to the latest RBA figures, private sector credit growth increased by 0.6% in September. The result was just above the generally expected figure of 0.5% but in line with August’s increase. On an annual basis, the growth rate increased from August’s rate of 4.7% to 5.3%.

“The surprise was from business credit…Given any precautionary shoring up of balance sheets from businesses was likely complete by September, this to us suggests some early signs that business investment might be meaningfully lifting,”said ANZ senior economist Adelaide Timbrell.

Commonwealth bond yields jumped on the day, not because of the report or September’s sales figures private credit figures but because the RBA did not defend its April 2024 ACGB yield target. By the end of the day, the 3-year ACGB yield had gained 7bps to 1.40%, the 10-year rate had jumped 25bps to 2.12% while the 20-year yield finished 22bps higher at 2.63%.

Owner-occupier loans accounted for about two-thirds of the net growth over the month, with business loans accounting for a good chunk of the balance. Investor loans again grew quite modestly while total personal debt contracted again.

The traditional driver of loan growth rates, the owner-occupier segment, grew by 0.7% over the month, slightly slower than August’s 0.8% increase. The sector’s 12-month growth rate sped up from August’s revised rate of 8.4% to 8.7%.

Lending in the business sector expanded by 0.7%, slightly more than August’s 0.6% increase. The segment’s annual growth rate increased from August’s 3.4% to 4.6%.

Monthly growth in the investor-lending segment slowed to a halt in early 2018. Shortly into the 2019/20 financial year, monthly growth rates slipped into the red before posting a series of flat or near-flat results until late 2020. Growth rates became positive again from December 2020. In September, net lending grew by 0.3%, in line with August’s revised rate. The 12-month growth rate increased from August’s rate of 2.2% to 2.4%.

Total personal loans contracted by 0.6% in September following a similar-sized fall in August, with the annual contraction rate slowing from 5.6% to 5.3%. This category of debt includes fixed-term loans for large personal expenditures, credit cards and other revolving credit facilities.