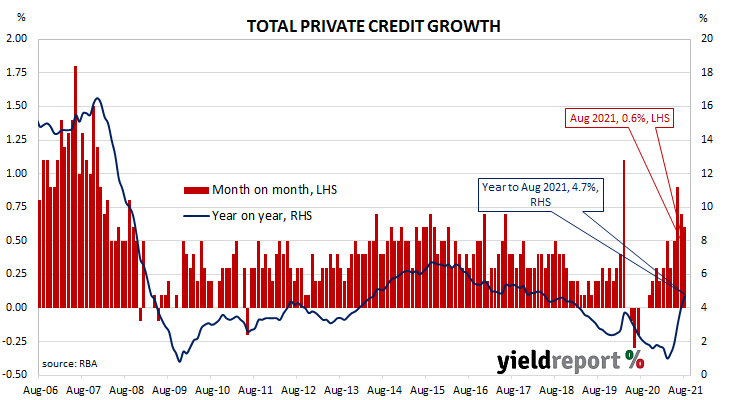

Summary: Private sector credit grows by 0.6% in August, just above expected figure; annual growth rate rises from 4.1% to 4.7%; businesses currently accessing credit lines to boost cash; owner-occupiers, business loans again mostly account for net growth; investor loans up modestly again, personal loans down; housing loan growth “elevated”, outstripping income growth, thus a concern for RBA.

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since late-2015. Private sector credit growth appeared to have stabilised in the September quarter of 2018 only to deteriorate through to the end of 2019. The early months of 2020 provided some positive signs but they disappeared in April 2020. Recent months’ figures indicate the downtrend is over.

According to the latest RBA figures, private sector credit growth increased by 0.6% in August. The result was just above the generally expected figure of 0.5% but just under July’s 0.7%. On an annual basis, the growth rate increased from July’s revised rate of 4.1% to 4.7%.

“As we have highlighted previously, businesses are currently accessing credit lines in much greater numbers in orders to boost cash flows. This is in response to the Bondi delta outbreak which sent New South Wales and Victoria back into lockdown,” said Westpac senior economist Andrew Hanlan.

Commonwealth Government bond yields moved a touch higher on the day. By the close of business, 3-year and 10-year ACGB yields had each inched up 1bp to 0.48% and 1.52%. The 20-year yield finished unchanged at 2.16%.

Owner-occupier loans and business loans accounted for most of the net growth over the month. Investor loans again grew quite modestly while total personal debt contracted again.

The traditional driver of loan growth rates, the owner-occupier segment, grew by 0.8% over the month, slightly slower than July’s 0.9% increase. The sector’s 12-month growth rate sped up from July’s revised rate of 7.9% to 8.4%.

Lending in the business sector slowed as business credit expanded by 0.6%, slightly more than half the rate of July’s 1.1% increase. The segment’s annual growth rate increased from July’s 2.4% to 3.4%.

Monthly growth in the investor-lending segment slowed to a halt in early 2018. Shortly into the 2019/20 financial year, monthly growth rates slipped into the red before posting a series of flat or near-flat results until late 2020. Growth rates became positive again from December 2020. In August, net lending grew by 0.2%, in line with July’s revised rate. The 12-month growth rate increased from July’s revised rate of 1.9% to 2.2%.

Total personal loans contracted by 0.6% in August following a 1.0% decrease in July, with the annual contraction rate slowing from 5.9% to 5.6%. This category of debt includes fixed-term loans for large personal expenditures, credit cards and other revolving credit facilities.

ANZ senior economist Adelaide Timbrell noted housing credit growth was “elevated” and “will likely continue to outstrip income growth, which the RBA has consistently said is a concern for them.”