Summary: Melbourne Institute inflation index rises in November; annual rate back to 1.4%.

Despite the RBA’s desire for a higher inflation rate, ostensibly to combat recessions, attempts to accelerate inflation through record-low interest rates have failed to date. The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower; the “coronavirus recession” then crushed it in the June quarter.

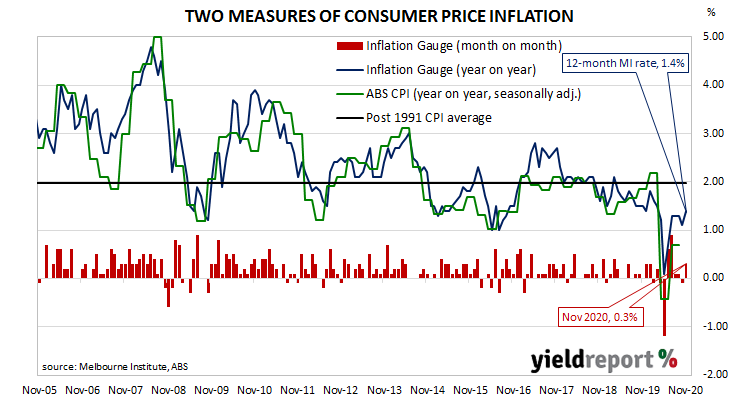

The Melbourne Institute’s latest reading of its Inflation Gauge index increased by 0.3% in November. The rise follows a 0.1% decline in October and 0.1% increases in both September and August. On an annual basis, the index rose by 1.4%, an acceleration from October’s comparable figure of 1.1%.

Long-term Commonwealth bond yields remained unchanged on the day, ignoring lower US Treasury yields at the close of trading on Friday night. At the close of business, 3-year, 10-year and 20-year ACGB yields finished at 0.17%, 0.90% and 1.54% respectively.

The Melbourne Institute’s Inflation Gauge is an attempt to replicate the ABS consumer price index (CPI) on a monthly basis. It has turned out to be a reliable leading indicator of the CPI, although there are periods in which the Inflation Gauge and the CPI have diverged for as long as twelve months. On average, the Inflation Gauge’s annual rate tends to overestimate the ABS headline rate by an average of a little under 0.1%.

Central bankers desire a certain level of inflation which is “sufficiently low that it does not materially distort economic decisions in the community” but high enough so it does not constrain “a central bank’s ability to combat recessions.” Hence the obsession among central bankers to increase inflation.