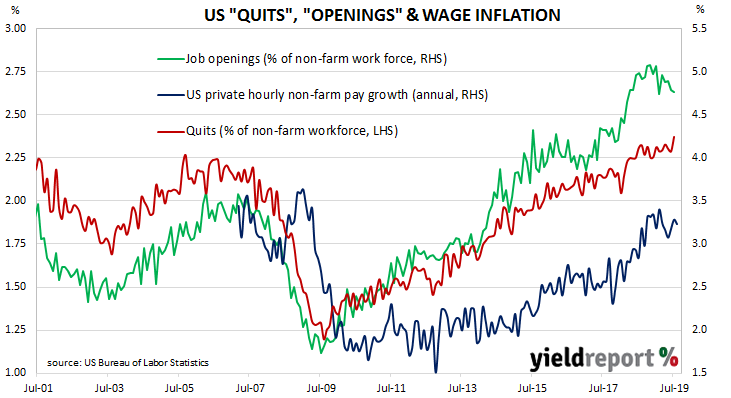

The quit rate as a percentage of total US non-farm employment had been rising slowly but steadily since the end of the GFC. It peaked in August 2018, stabilised and then remained largely unchanged through the remainder of 2018 and into 2019 at a historically high level. Despite international factors and some US surveys casting doubts on future economic conditions, the latest figures have continued in this fashion.

Figures released as part of the most recent JOLTS report show the quit rate has hit a new series high in July. 2.4% of the non-farm workforce left their jobs voluntarily in July, having registered 2.3% in each of the previous months from June 2018. Quit numbers were highest in the health care/social assistance and professional/business services sectors while the retail trade and durable goods sectors recorded the largest falls. Overall, the total number of quits increased from June’s revised figure of 3.462 million to 3.592 million in July.

ANZ economist Jack Chambers said the high rate illustrated workers’ confidence in their ability to find a new job.

Total job openings fell for a second consecutive month. Total vacancies during July fell by 31,000 from June’s revised figure of 7.284 million to 7.217 million, driven by reduced openings in the wholesale trade, professional/business services and health care/social assistance sectors. Additional openings in the construction and information sectors provided some offset to the fall but, overall, 10 out of 19 sectors experienced fewer job openings than in the previous month.

US Treasury bond yields had been rising significantly in the days prior to the report’s release, apparently as part of a broad movement in yields prior to the ECB’s policy meeting later in the week. This trend continued and Treasury bond yields finished the day noticeably higher. By the close of US trade, 2-year Treasury yields were 7bps higher at 1.67% while 10-year and 30-year yields had each gained 9bps to 1.73% and 2.22% respectively.