Since late 2017/early 2018, a very clear downtrend has been evident in the monthly figures of both the number and value of home loan commitments. After the figures from February were released, some economists speculated the worst may have been over. After the Coalition Government retained power in May, economists began to expect a greater demand for mortgages. The RBA then cut official rate in June and July, increasing the attractiveness of property.

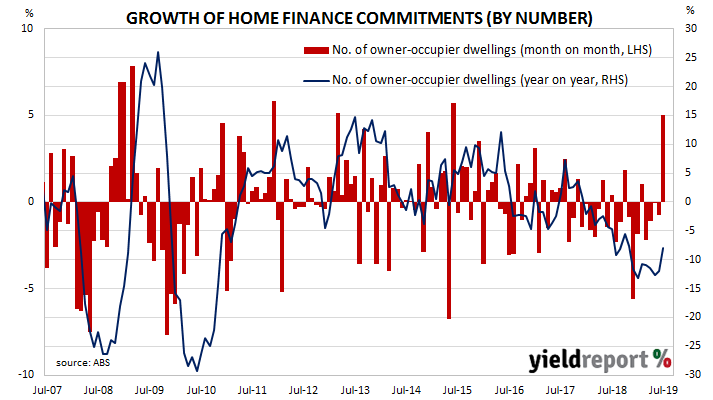

July’s housing finance commitment figures have now been released and they were noticeably higher than expected. The total number of loan commitments to owner-occupiers jumped by 5.0%, a marked turnaround from June’s revised figure of -0.8%. On an annual basis, the growth rate recovered from June’s revised figure of -12.0%, recording -8.0%. When “re-financings” are removed, the number of loan commitments increased by 5.3% over the month, well in excess of the expected 1.5% increase but also 8.3% lower than in July 2018.

Westpac senior economist Matthew Hassan said the turnaround came a month earlier than expected. “While the July data came in above expectations, the surprise relates more to the timing of the lift for the finance data rather than the market upturn itself…” He said other indicators had recently shown an increase in “momentum in August after having stabilised in June-July.”

Despite the surprise, bond yields finished the day lower across the curve, even though the US 2-year Treasury yield had increased a little and its 10-year yield had remained unchanged. By the end of the day, the yield on 3-year ACGBs had lost 2bps to 0.81%, while 10-year and 20-year yields had both shed 6bps to 1.04% and 1.44% respectively.

Reactions in the cash futures market were subdued but expectations of future rate cuts softened. At the close of trade, October contracts implied another 25bps rate cut was a 41% chance, down from the previous day’s 47%. The likelihood of a rate cut at the RBA’s November meeting was essentially the same, having slipped from 94% to 92%. At this level, a third rate cut for the year is still deemed to be highly likely.

In dollar terms, total loan approvals excluding refinancing increased by 5.1% over the month after having increased by 3.2% in June. However, on a year-on-year basis, total approvals excluding refinancing were still 11.8% lower but it was still an improvement on June’s comparable figure of -17.2% after revisions.