Summary: Value of loan commitments up 1.5% in February, slightly less than expected; 13.3% higher than February 2023; ANZ: sales volumes up since January, suggests lending should continue growing; ACGB yields up noticeably; rate-cut expectations soften; update suggests dent from November rate rise was milder than initial estimates had indicated; value of owner-occupier loan approvals up 1.6%; investor approvals up 1.2%; number of owner-occupier home loan approvals up 0.9%.

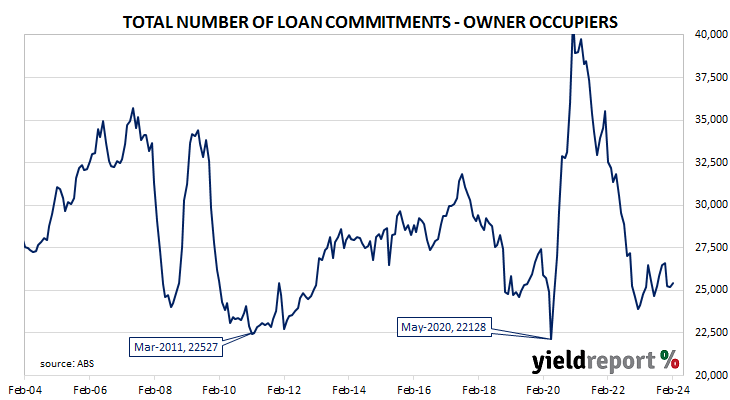

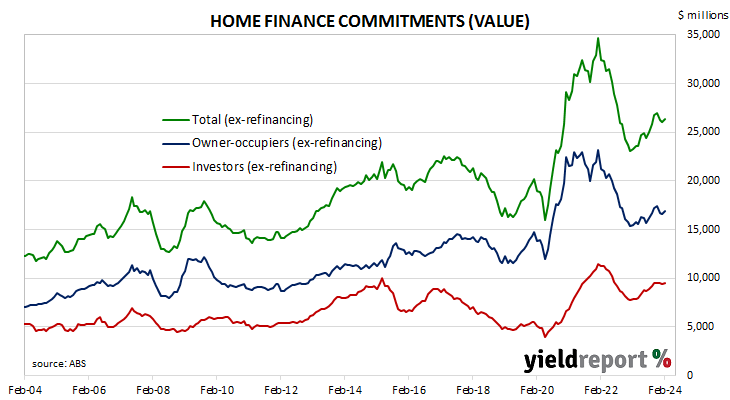

The number and value of home-loan approvals began to noticeably increase after the RBA reduced its cash rate target in a series of cuts beginning in mid-2019, potentially ending the downtrend which had been in place since mid-2017. Figures from February through to May of 2020 provided an indication the downtrend was still intact but subsequent figures then pushed both back to record highs in 2021. However, there has been a considerable pullback since then, although the total value of new loans is still elevated by historical standards.

February’s housing finance figures have now been released and total loan approvals excluding refinancing increased by 1.5% In dollar terms over the month, slightly less than the 2.0% rise which had been generally expected and in contrast with January 0.8% fall after revisions. On a year-on-year basis, total approvals excluding refinancing were 13.3% higher than February 2023, up from the previous month’s comparable figure of 12.8%.

“Sales volumes have picked up since January suggesting lending should continue to grow in coming months,” said ANZ senior economist Blair Chapman.

Commonwealth Government bond yields rose noticeably on the day, largely in line with movements of US Treasury yields on Friday night. By the close of business, the 3-year ACGB yield had gained 8bps to 3.73%, the 10-year yield had increased by 10bps to 4.21% while the 20-year yield finished 9bps higher at 4.51%.

In the cash futures market, expectations regarding rate cuts in the next twelve months softened. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.305% through May and 4.29% in June. However, August contracts implied a 4.22% average cash rate, November contracts implied 4.09%, while February 2025 contracts implied 3.95%, 37bps less than the current rate.

“Overall, the update and revised profile suggests the dent from November’s rate rise was a little milder than initial estimates had indicated with the gradual up-trend in approvals looking more intact,” said Westpac senior economist Matthew Hassan. “That said momentum is still sluggish in most markets and notably softer in Victoria.”

The total value of owner-occupier loan commitments excluding refinancing increased by 1.6%, up from January’s 0.9% fall. On an annual basis, owner-occupier loan commitments were 9.1% higher than in February 2023, up from January’s comparable figure of 8.4%.

The total value of investor commitments excluding refinancing increased by 1.2%. The rise follows a 0.8% decline in January, taking the growth rate over the previous 12 months from 21.7% to 21.5%.

The total number of loan commitments to owner-occupiers excluding refinancing increased by 0.9% to 24447 on a seasonally adjusted basis, in contrast with January’s 0.3% decline. The annual growth rate slowed a touch from 5.6% after revisions to 5.5%.