No one really expected the RBA to change the official cash rates at its October meeting and when the announcement of no change was made at 2.30pm, barely a ripple was registered in financial markets. Prior to the meeting, the probability of a cut to 1.25% implied by October cash contracts was 4% because economists and other observers all have their eyes on November’s meeting.

There are only four distinct months of the year where the RBA is thought to considering changing rates, barring emergencies. Each of these months follow the release of CPI figures, which are released on a quarterly basis as well as the quarterly Statement on Monetary Policy. June quarter CPI figures are released in July, September quarter CPI figures are released in October and so on. For a central bank which has essentially two priorities, one being employment and the other being price stability, consumer inflation figures are very important. So, it is no surprise the RBA would wait until the latest inflation data is out before moving one way or another. Therefore rate decisions, more often than not, are made in February, May, August and November.

Westpac’s Bill Evans noted the move to a neutral bias in the Governor’s statement and how the implied reference to the next CPI report present in July statement is not present in this one. “…the decision to de-link the next inflation report from next month’s policy decision must be partly influenced by developments in the housing market.” NAB’s David de Garis disagreed regarding the link to the next inflation report. “The next big local data point that could yet make the upcoming November meeting a “live” meeting is the September quarter CPI, being released on 26 October. NAB’s model forecast is for steady underlying inflation of 0.5% q/q that would see the RBA continue to hold rates steady through the New Year.” ANZ, as with Westpac, noted the reference to housing. “The Bank is clearly mindful of the resurgence in house price strength, noting yesterday that “some markets have strengthened recently”. The looming swell in supply is also on the Bank’s radar, and yesterday’s smaller-than-expected fall in building approvals (after a 12% m/m rise in July) would have been noted.

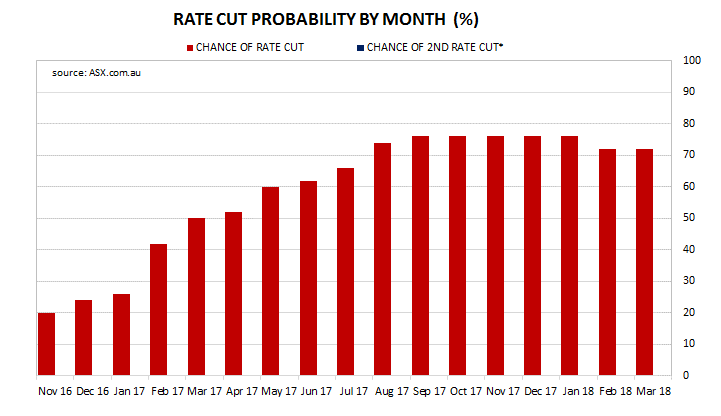

After the August cut from 1.75% to 1.50%, there were quite a few economists, strategist and others who expected another cut to 1.25% and beyond. On the day after the August decision, November cash contracts implied a 46% probability of another cut. Now, with only a month to go, the odds have been cut back to 1 in 5. 3 year and 10 year bond yields both rose 5bps to 1.57% and 2.08% respectively on the day.