February is one of the four months of the year in which rate changes traditionally occur, although the RBA can change the official rate on any day should it so choose. The February meeting, along with May, August and November meetings, follows a quarterly CPI release which may provide the impetus for the RBA board to act. In this case current CPI figures, along with other measures of inflation and economic activity, have not proved sufficiently weak for the RBA to act and it has left the official rate at 1.50%.

The RBA expects GDP growth to rebound in December, boosted by exports. On top of export growth, a moderate increase in consumption and higher non-mining investment are expected to keep GDP growth at around 3% for the next two years. Inflation forecasts have remained intact with wages growth to remain low.

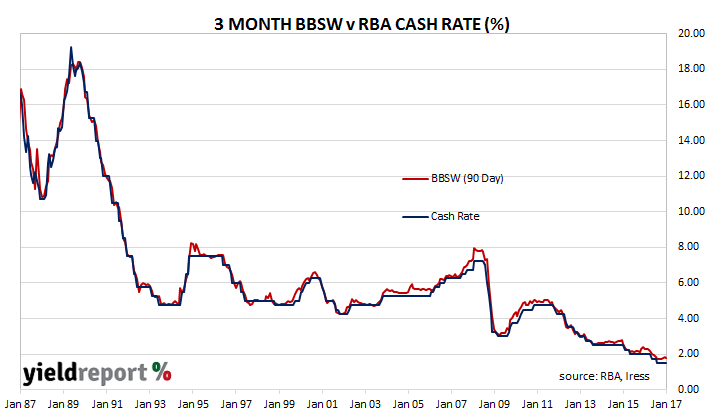

Reactions in bond and currency markets were somewhat contradictory. The Aussie went from 76.3 US cents to 76.8 before it fell back, while the 3 year bond yield fell 3bps to 1.95% and the 10 year bond yield fell from 2.795% to 2.725%. Prices in the cash market barely reacted; there’s still a slim chance a rate cut through to August 2017 and an increasing chance of a rate rise from October 2017.

Here’s what some economists thought about the RBA decision:

Ivan Colhoun, NAB

“The Statement seemed both a little more upbeat on the global growth outlook (conditions described as having improved in recent months) and reasonably relaxed about the Bank’s view of both the Australian growth outlook and an expected slow return of inflation to the target. The Bank would likely need to change one of these views significantly to alter its policy rate in the near term.”